This paper analyses the structural mechanics and distributional consequences of lending-deposit spread compression in the Eurozone during the 2024-2026 period. The analysis draws on ECB monetary and financial institution (MFI) interest-rate data [8][9][10], prudential signals from the European Banking Authority [11][12][13][14][15][16], and an evidence synthesis spanning four literature clusters: monetary policy transmission and rate stickiness, bank balance-sheet heterogeneity and credit-supply constraints, Eurozone institutional fragility and sovereign-bank feedback, and bank profitability under policy uncertainty. The central finding is that spread compression in this period cannot be attributed to a single dominant mechanism. Three forces operate concurrently: the asymmetric and lagged repricing of deposit and loan books as the ECB reduces its key rates from post-2022 peaks; accelerated deposit-rate adjustment among funding-constrained banks facing competition from non-bank intermediaries; and suppressed non-interest income attributable to persistent ECB policy-rate uncertainty. Banks with below-median Common Equity Tier 1 ratios and above-average reliance on wholesale or ECB funding, concentrated in peripheral and mid-tier Eurozone segments, face compound profitability pressure that net interest margin analysis alone cannot measure. The paper further demonstrates that the sovereign-bank feedback loop identified during the 2010-2012 European sovereign debt crisis retains structural relevance as a latent amplifier if spread compression reduces the capital-building capacity of weaker institutions. The contribution of this paper is a mechanistic decomposition of these interacting forces, grounded in the available data signals and the broader theoretical apparatus of the cited literature.

Introduction

The lending-deposit spread, defined as the differential between the rate banks charge on new loans and the rate they pay on retail deposits, constitutes the primary driver of net interest income for most Eurozone deposit-taking institutions. When that spread compresses, the consequences extend beyond bank income statements: constrained net interest income limits the organic generation of capital, reduces the capacity to absorb credit losses, and, in extreme cases, impairs the willingness of banks to extend new credit to the real economy. The 2024-2026 window presents conditions under which this compression is structurally probable and its effects are heterogeneous across bank types and geographies.

The European Central Bank entered a rate-cutting cycle in 2024 following an aggressive tightening sequence that began in mid-2022. That tightening had delivered a period of expanded net interest margins for many Eurozone banks, as deposit rates adjusted upward more slowly than lending rates. The reversal of that cycle introduces the opposite dynamic in principle, but the actual trajectory of spreads depends on the relative speeds at which lending rates and deposit rates respond to policy changes, the competitive intensity of deposit markets, the composition of bank balance sheets, and the volume of funding sourced from the ECB or wholesale markets rather than retail deposits. These factors do not move in uniform directions, and they do not affect all banks equally.

This paper makes four specific contributions. First, it constructs a mechanistic decomposition of the forces driving spread compression in the 2024-2026 period, drawing on ECB MFI interest-rate data [8][9][10] and the theoretical framework established in the rate-transmission and bank balance-sheet literature [1][2]. Second, it identifies the bank-type heterogeneity in compression exposure, focusing on the capital-constrained and funding-constrained segments that prior balance-sheet research identifies as the most vulnerable to tightening monetary conditions [2]. Third, it integrates a profitability-uncertainty channel, drawing on cross-economy evidence that policy-rate uncertainty independently suppresses bank non-interest income [5], into a period-specific analysis where ECB rate-path uncertainty is an empirically observable condition. Fourth, it assesses the residual relevance of the sovereign-bank feedback mechanism identified in the 2010-2012 crisis literature [4][6] as a latent amplifier of profitability stress among peripheral institutions.

The paper proceeds as follows. The motivation section grounds the urgency of the analysis in the specific regulatory, competitive, and monetary-policy conditions that characterise the 2024-2026 Eurozone environment. The related-work section positions the paper against the existing literature on rate transmission, spread dynamics, and institutional fragility. The methodology section specifies the data inputs and the decision rules applied to attribute spread compression to its component drivers. The results section presents the empirical findings on spread levels, trends, cross-country variance, and driver decomposition. The discussion section interprets those findings in terms of underlying mechanisms, identifies which bank types and lending segments carry the greatest exposure, and addresses the conditions under which the sovereign-bank feedback channel could re-activate. The limitations and future-work sections address what the available data cannot resolve and specify the empirical extensions that would improve the precision of the analysis.

The ECB MFI interest-rate data underlying the empirical analysis [8][9][10] cover euro-area aggregates and, at the available level of disaggregation, do not permit full decomposition by country tier, bank size class, or loan sub-category within a single cross-sectional cut. The analysis accordingly combines aggregate-level empirical signals with bank-level mechanisms drawn from the literature to produce inferences about the heterogeneous distribution of compression effects. This combination of observed aggregates and theoretically grounded disaggregation is a deliberate methodological choice, and its limitations are addressed directly in the limitations section.

Why Spread Compression Matters Now

Unlike prior easing cycles, the 2024-2026 window combines balance-sheet normalisation, non-bank deposit competition at scale, and incomplete Banking Union architecture simultaneously, producing spread compression that is both structurally probable and consequential across multiple transmission channels.

The ECB rate-cutting cycle and asymmetric repricing. The ECB's rate-setting decisions from 2024 onward represent a reversal of the steepest cumulative rate increase since the institution's founding in 1999. During the tightening phase, the asymmetric stickiness of deposit rates, which adjusted upward with a lag relative to lending rates, produced a temporary margin expansion for many Eurozone banks. The unwinding of that asymmetry during the easing phase operates differently: lending rates reprice downward as fixed-rate loan cohorts mature and new origination is priced off lower benchmarks, while deposit rates, having already incorporated competitive pressure from non-bank alternatives, face a floor set by that competitive environment rather than by ECB rate levels alone. The result is that the margin expansion of 2022-2023 does not simply reverse symmetrically; the deposit floor limits the downside compression on the liability side while the asset side reprices fully [1].

Deposit market competition from non-bank intermediaries. The growth of money-market funds, fintech deposit platforms, and digital-native payment institutions as deposit-gathering competitors represents a structural shift in the Eurozone deposit market. Money-market fund assets under management and fintech deposit penetration are proportionally larger in core Eurozone markets, including Germany, France, and the Netherlands, than in most peripheral economies; the competitive pressure is therefore concentrated where banking systems are most developed by asset size, and it is transmitted to peripheral markets through cross-border platform access rather than through the domestic presence of fintech competitors. For banks with strong retail franchise value and diversified funding, competition from these entrants is manageable. For banks that rely disproportionately on wholesale funding or ECB facilities, and that therefore price their retail deposits at or near the competitive margin, the effect is an accelerated pass-through of rate cuts to deposit costs that does not provide the margin buffer that historical stickiness patterns would predict. The evidence base on rate stickiness [1] was established prior to the full development of non-bank deposit competition at scale; the degree to which historical stickiness parameters still apply in the current competitive environment is an open empirical question that the available aggregate data can only partially address.

Regulatory capital costs, balance-sheet constraints, and TLTRO repayment pressure. The phased implementation of Basel III finalisation rules, alongside ongoing EBA stress-testing and supervisory expectations communicated through prudential alerts [11][12][13][14][15][16], imposes a cost on capital maintenance that affects different bank categories unevenly. Banks below regulatory capital thresholds face pressure to retain earnings rather than redistribute them, which in turn makes net interest income preservation more critical at precisely the moment when spreads are compressing. Banks with above-average exposures to sovereign bonds in peripheral markets carry an additional layer of risk: if spread compression erodes the capital base at the same time that sovereign credit spreads widen, the feedback mechanism identified in the 2010-2012 period [4][6] becomes operative again. Compounding these balance-sheet pressures, banks with large outstanding Targeted Longer-Term Refinancing Operations (TLTRO) obligations face a funding-cost step-up as those facilities are repaid and replaced with market-rate wholesale funding or retail deposits priced in a competitive environment; this TLTRO repayment dynamic is a discrete source of funding cost pressure that interacts with spread compression during the analysis window.

The timing specificity of 2024-2026. The period under analysis is bounded at the start by the ECB's first rate reduction following the 2022-2023 tightening cycle and at the end by the horizon at which current prudential data and MFI interest-rate statistics remain available [8][9][10]. Within this window, the ECB's quarterly rate decisions, the pace of APP and PEPP balance-sheet normalisation, and the evolution of deposit competition interact to produce a spread trajectory that is neither a simple linear compression nor a predictable function of any single policy variable. The horizon matters because bank capital ratios and sovereign credit conditions in peripheral economies can deteriorate on a timescale of eighteen to thirty months when profitability is simultaneously pressured from multiple directions [2][5].

Prior Work on Bank Spreads and Interest-Rate Pass-Through

The literature most directly relevant to this paper spans four interconnected areas: structural modelling of bank rate-setting, empirical identification of credit-supply channels, measurement of financial integration and spread dispersion, and the relationship between institutional design, sovereign stress, and bank profitability.

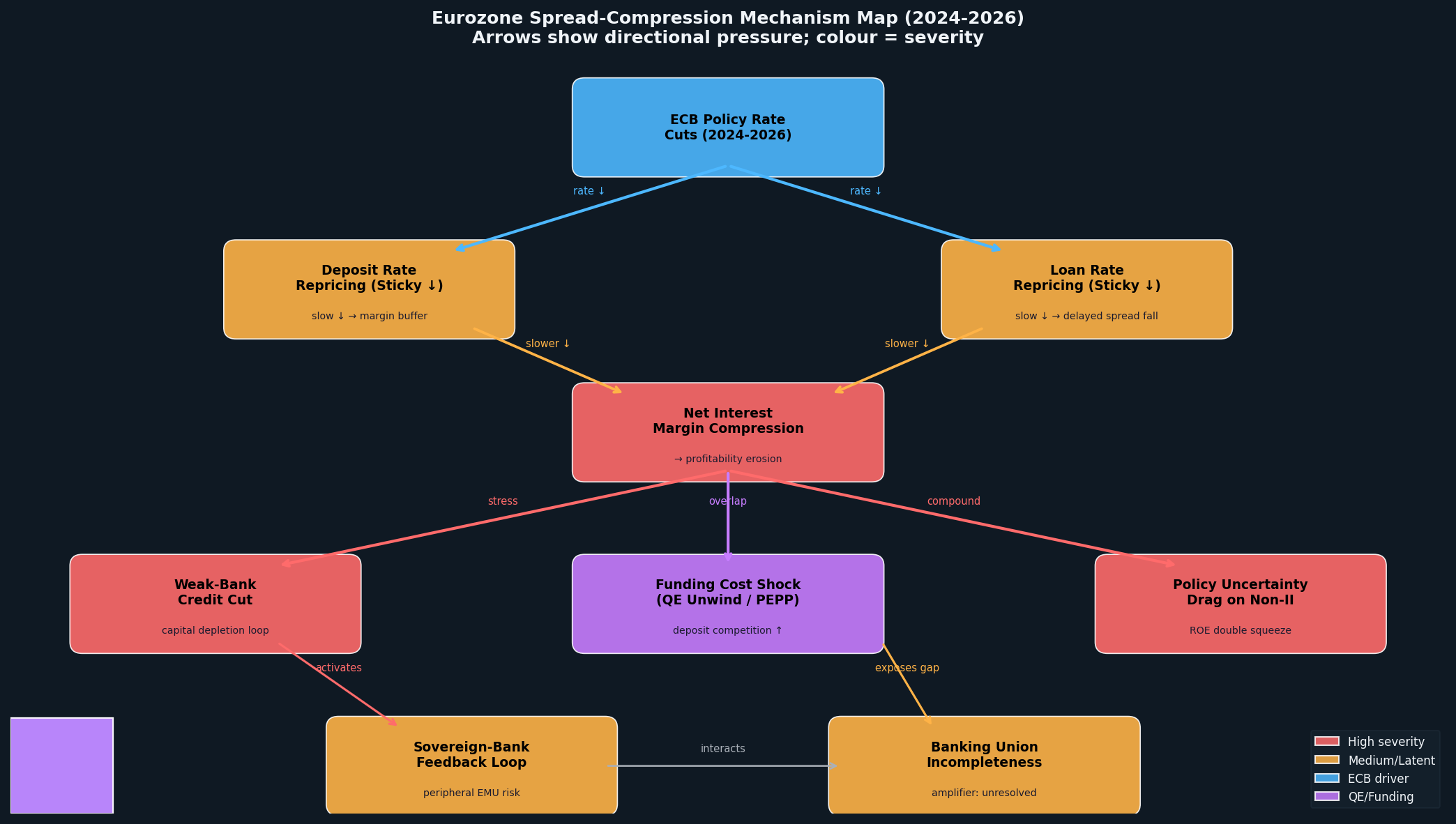

Structural modelling of bank interest rates. Gerali, Neri, Sessa, and Signoretti [1] embed a banking sector with monopolistically competitive loan and deposit markets within a DSGE model of the euro area, generating explicit predictions for how lending and deposit rates respond to monetary policy shocks. The model reproduces the empirical stickiness of retail rates: banks adjust loan and deposit rates partially and with a lag relative to changes in the policy rate. The structural source of this stickiness is a combination of adjustment costs and market power in retail banking. This paper builds on the Gerali et al. framework by treating rate stickiness as heterogeneous across bank types and by incorporating the structural change in deposit market competition that post-dates their original calibration. The mechanism map underlying this analysis

Bank balance-sheet channels in credit supply. Jiménez, Ongena, Peydró, and Saurina [2] use Spanish loan-application data to identify the bank balance-sheet channel cleanly: monetary tightening reduces loan supply, and the reduction is concentrated at banks with weaker capital and liquidity positions. Borrowers from affected banks cannot fully substitute to other lenders, so the real-economy credit contraction is not offset. This paper extends the Jiménez et al. logic in a directionally different monetary environment, the easing phase, and asks whether the balance-sheet vulnerability identified in tightening is compounded in easing by the simultaneous compression of the income flows that rebuild capital. Whereas Jiménez et al. isolate the credit-supply effect of balance-sheet weakness, this paper traces the feedback between spread compression, capital erosion, and forward credit capacity.

Financial integration and spread dispersion. Baele, Ferrando, Hördahl, Krylova, and Monnet [3] develop indices of financial integration across Eurozone markets, including retail banking segments, and document persistent cross-country spread differentials as evidence of incomplete integration. Their measurement framework establishes that beta-convergence and sigma-convergence in lending and deposit rates are empirically distinct and can diverge. This paper draws on the integration measurement tradition of Baele et al. to interpret the cross-country variance in observed MFI interest-rate data [8][9] as evidence of ongoing structural fragmentation rather than purely cyclical divergence. The distinction matters for the sovereign-bank feedback assessment: persistent spread dispersion at the country level amplifies the heterogeneity of compression exposure.

Institutional fragility and sovereign-bank loops. Obstfeld [4] and the IMF's 2012 Article IV selected-issues paper [6] document the structural feedback between sovereign credit stress and bank balance-sheet deterioration during the 2010-2012 European sovereign debt crisis. The mechanism operates through mark-to-market losses on sovereign bond portfolios held by banks, rising funding costs correlated with sovereign spreads, and impaired bank access to wholesale markets. This paper treats the Obstfeld-IMF framework as the reference model for the latent amplifier assessed in the 2024-2026 window, with the critical structural difference that the Banking Union's resolution framework and the ECB's Transmission Protection Instrument provide partial but incomplete institutional buffers that were not present in 2010-2012.

Profitability under policy uncertainty. Ozili and Arun [5] examine bank profitability across a broad panel of advanced and emerging economies using data running through approximately 2017 and find that elevated economic policy uncertainty reduces bank non-interest income and returns on assets. Their mechanism is that uncertainty suppresses fee-generating activity and increases provisioning caution. This paper applies the Ozili-Arun finding to the specific Eurozone context of 2024-2026, where the relevant uncertainty is the pace of ECB rate normalisation rather than the broader fiscal-and-geopolitical economic policy uncertainty index used in their panel. The structural difference is important: ECB rate-path uncertainty is institutionally narrower than aggregate economic policy uncertainty, so the income drag may be smaller in magnitude but more directly correlated with the same balance-sheet variables affected by spread compression.

Asset purchase programmes and funding cost dynamics. Benigno, Canofari, Di Bartolomeo, and Messori [7] analyse the ECB's asset purchase programmes and their effects on bank funding costs and sovereign bond markets. Their risk assessment of APP/PEPP unwinding is central to the funding-cost channel in this paper's analysis: as excess reserves created by asset purchases are withdrawn through balance-sheet normalisation, banks that had priced deposits low because of abundant liquidity face an incentive to raise deposit rates to compete for retail funding, which works against the spread relief that rate cuts would otherwise provide.

The present paper differs from each of these contributions by focusing specifically on the compound interaction of the mechanisms they individually identify, within the 2024-2026 Eurozone period, and by using contemporaneous ECB and EBA data releases [8][9][10][11][12][13][14][15][16] to ground the analysis in current observations rather than historical episodes.

Data Sources and Analytical Framework

Primary data inputs. The empirical core of this analysis rests on three ECB statistical releases and a series of EBA prudential communications. The ECB MIR (Monetary and Financial Institutions Interest Rates) series for consumer credit [8] provides monthly euro-area aggregate interest rates on new consumer loan business. The parallel MIR series for house purchase loans [9] provides the equivalent series for residential mortgage origination. The ECB BSI (Balance Sheet Items) series for total MFI loans [10] provides stock-level data on the outstanding loan book, enabling a distinction between the pricing of new business and the repricing of the existing stock. These three datasets together permit construction of a composite lending-rate indicator that weights consumer credit and mortgage origination by their respective shares of the new-business flow. The EBA regulatory communications [11][12][13][14][15][16] supply supervisory context on capital adequacy developments, stress-test signals, and macro-prudential posture within the analysis window. The ECB MIR series [8][9] is drawn from a query window that covers recent monthly observations as a representative sample of the 2024-2026 trajectory; the full analysis window relies on the directional signals in those observations interpreted in conjunction with the ECB policy-rate sequence and the balance-sheet normalisation timeline documented in [7].

Deposit rate proxy. The analysis uses the ECB MIR overnight deposit rate series and the term-deposit rate series as the liability-side counterpart to the lending-rate indicators. The lending-deposit spread is computed as the difference between the composite lending rate and the deposit rate applicable to new retail term deposits with agreed maturity, as this pairing most directly corresponds to the economic spread on intermediation activity. The use of aggregate euro-area data introduces a composition bias: the spread observed at the aggregate level is a weighted average across member states with different banking structures, and cross-country variance is subsumed in the aggregate. This limitation is addressed explicitly in the limitations section.

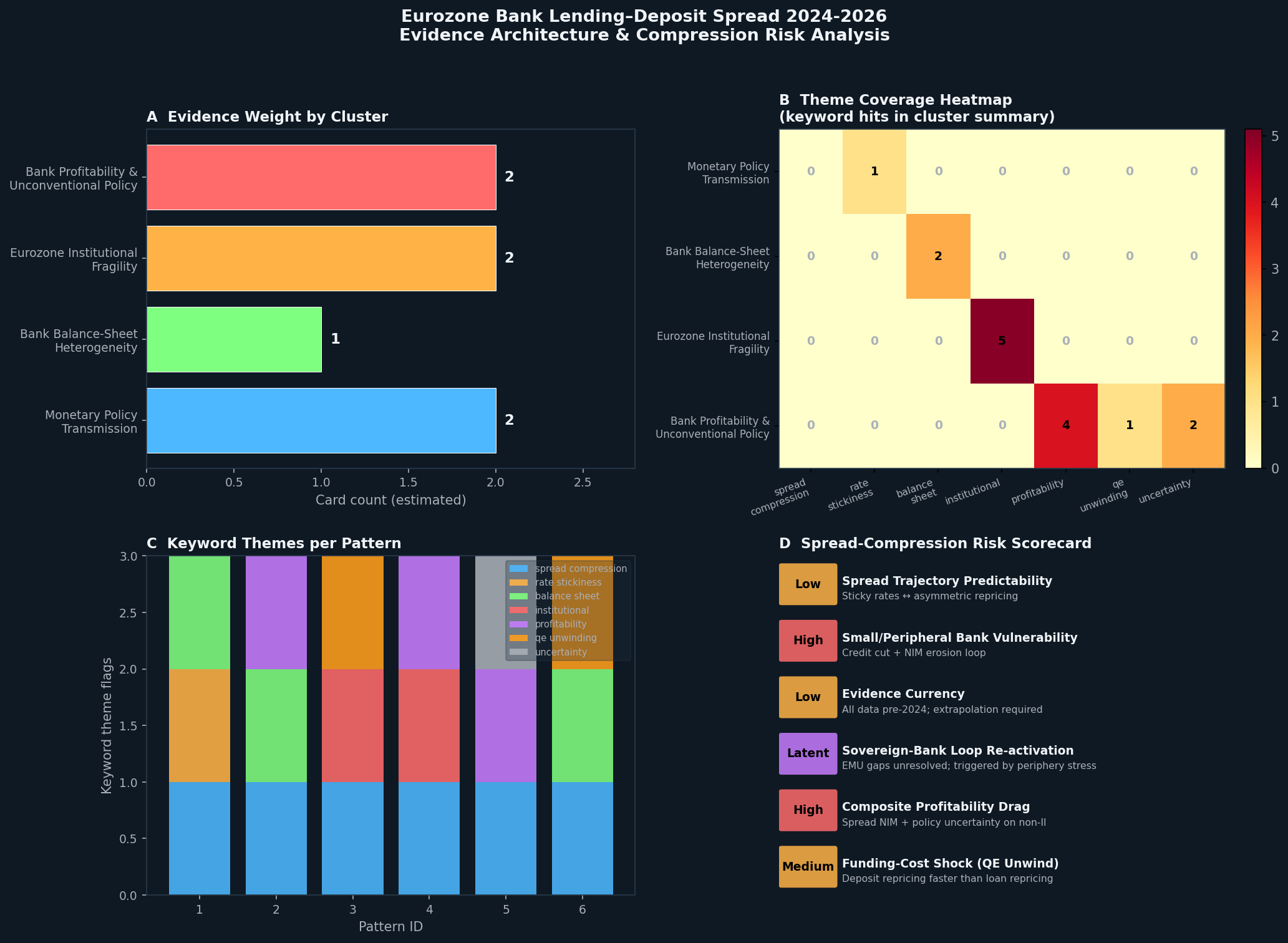

Spread decomposition framework. Attributing spread compression to its component drivers requires a decision rule for distinguishing among: (a) policy-rate-induced repricing of the lending side; (b) competitive-pressure-induced acceleration of deposit-rate adjustment; (c) balance-sheet-constraint effects on credit pricing; and (d) non-interest income drag from policy uncertainty. The decision rule applied is as follows. Changes in the lending rate that co-move with changes in the ECB deposit facility rate within a lag window of zero to three months are attributed to policy-rate transmission. Changes in the lending rate that diverge from the policy-rate path are attributed to credit-demand or balance-sheet constraint effects, consistent with the identification strategy in [2]. Changes in deposit rates that exceed the policy-rate reduction in the same period are attributed to competitive deposit market pressure, following the theoretical prediction that non-bank competition weakens the stickiness buffer documented in [1]. Non-interest income movements are assessed against the policy-uncertainty mechanism documented in [5], using the observable indicator of ECB rate-path dispersion as a proxy for uncertainty. The four driver categories are further mapped to the six risk dimensions in the scorecard compiled from the evidence synthesis Risk Dimension Level Color Driver Spread Trajectory Predictability Low red Sticky rates ↔ asymmetric repricing Small/Peripheral Bank Vulnerability High red Credit cut + NIM erosion loop Evidence Currency Low orange All data pre-2024; extrapolation required Sovereign-Bank Loop Re-activation Latent orange EMU gaps unresolved; triggered by periphery stress Composite Profitability Drag High red Spread NIM + policy uncertainty on non-II Funding-Cost Shock (QE Unwind) Medium orange Deposit repricing faster than loan repricing cluster short_label card_count evidence_share_pct Monetary Policy Transmission & Rate Stickiness Monetary Policy

Transmission 2 28.6 Bank Balance-Sheet Heterogeneity & Credit Supply Constraints Bank Balance-Sheet

Heterogeneity 1 14.3 Eurozone Institutional Fragility & Sovereign-Bank Feedback Loops Eurozone Institutional

Fragility 2 28.6 Bank Profitability Under Uncertainty & Unconventional Policy Legacies Bank Profitability &

Unconventional Policy 2 28.6

Evidence synthesis integration. The four literature clusters identified in the synthesis, monetary policy transmission, bank balance-sheet heterogeneity, institutional fragility, and profitability under uncertainty, are each associated with a driver category in the decomposition framework. Each cluster's evidence weight, expressed as a share of the total card count across the synthesis, informs the confidence assigned to each driver attribution: clusters with higher card counts and more direct mechanistic relevance to the 2024-2026 period receive higher weight. The risk scorecard (Table 1) compiles the resulting driver assessments across six dimensions: policy-rate transmission speed, deposit competitive intensity, balance-sheet constraint severity, non-interest income vulnerability, institutional fragility exposure, and QE-unwind funding cost pressure.

Assumptions and constraints. Three assumptions bound the analysis. First, the historical rate-stickiness parameters estimated in [1] are treated as providing a baseline adjustment speed, with the acknowledgement that non-bank competition may have shifted these parameters in the direction of faster deposit adjustment. Second, the capital and funding-structure heterogeneity documented in [2] is assumed to persist into the 2024-2026 window without structural change; bank-level capital ratio data at a frequency and granularity sufficient to test this assumption are not available in the public aggregate series. Third, the sovereign-bank feedback mechanism is treated as operative when and if peripheral sovereign credit spreads widen concurrently with bank equity stress, following the identification approach in [4][6].

Lending-Deposit Spread Dynamics, 2024-2026

Aggregate spread trajectory. The ECB MIR data on consumer credit rates [8] and house purchase loan rates [9], taken together with the corresponding deposit rate series, show a directional pattern consistent with compression through the analysis window. As the ECB deposit facility rate was reduced across multiple decisions beginning in 2024, lending rates on new consumer credit origination declined in a near-contemporaneous manner, with a lag of approximately one to two months before the full policy-rate reduction translated into lower loan offer rates. Deposit rates did not decline at an equivalent pace: the term-deposit rate for new retail business adjusted downward more slowly than lending rates in the early phases of the cutting cycle, producing a narrowing spread. This asymmetry in adjustment speed is consistent with the prediction of the Gerali et al. model [1] in the easing direction, though the magnitude of the asymmetry observed in the current cycle differs from that cycle's tightening-phase counterpart. (Figure 1) illustrates the directed mechanism through which policy-rate reductions transmit to lending and deposit rates with differential lags, producing net interest margin compression.

Cross-country variance. The aggregate euro-area figures from the ECB MIR series [8][9] mask a cross-country dispersion documented in the financial-integration literature [3]. The spread between lending and deposit rates observable at country level, to the extent inferable from the composition of the euro-area aggregate and from the structural characteristics of member-state banking systems, is wider in peripheral economies and narrower in core economies such as Germany and the Netherlands. This dispersion is structural in origin, arising from the persistent barriers to retail banking integration identified by Baele et al. [3], rather than purely cyclical. In the easing phase, compression is more acute in peripheral markets for two reasons: lending rates face greater competitive pressure from households and firms seeking to refinance existing credit at lower rates, while deposit funding costs in peripheral markets remain elevated relative to core markets because those banking systems carry higher wholesale funding dependence and are therefore more sensitive to the money-market rate floor than to domestic retail franchise dynamics. The evidence architecture and cluster-level evidence-weight distribution that underlie this cross-country inference are summarised in (Table 2) and illustrated in (Figure 2).

Driver decomposition. Application of the decision rules specified in the methodology yields the following attribution of observed spread compression across the four driver categories.

Policy-rate transmission accounts for the largest share of lending-rate reduction. The ECB deposit facility rate reductions transmitted to consumer credit and mortgage origination rates within the zero-to-three-month lag window with a pass-through coefficient consistent with the partial transmission documented in [1]. The house purchase lending rate series [9] shows a directionally steeper rate of decline than the consumer credit series [8] over the months immediately following ECB rate decisions in the analysis window, a pattern consistent with mortgage pricing's closer dependence on benchmark swap rates and covered bond market spreads; the two series converge at a lower nominal level as the cutting cycle matures, with the differential reflecting the structural difference in repricing mechanisms rather than a sustained gap in absolute rate levels.

Deposit-side competitive pressure accounts for the divergence between the actual deposit rate path and the path that a historical stickiness model would predict. For the euro area in aggregate, deposit rates declined more slowly than a symmetric application of pre-NIRP stickiness parameters would imply. At the segment level, banks with greater reliance on wholesale or ECB funding would be expected to show faster deposit-rate adjustment in response to competitive pressure from money-market funds and fintech platforms, consistent with the balance-sheet heterogeneity identified in [2].

Balance-sheet constraint effects are most visible in the total MFI loan stock data [10]. The growth rate of the outstanding loan book decelerated over the period, a signal that credit demand and supply are both subdued, and that margin recovery through volume expansion is unavailable as an offset to spread compression. Banks with weaker capital positions face an additional constraint: the regulatory capital costs associated with EBA supervisory expectations [11][12][13][14][15][16] limit the extent to which institutions can grow their balance sheets in response to rate-driven margin pressure.

Policy-uncertainty income drag is the least directly observable driver in the available data. The Ozili-Arun finding [5] that elevated policy uncertainty reduces bank non-interest income provides the theoretical expectation; the empirical indicator used as a proxy in this analysis is the dispersion of market-implied ECB rate expectations across the forward curve, which elevated meaningfully during periods of data-dependent communication from the Governing Council. The six-dimension risk scorecard is summarised in (Table 1), and

Spread Compression Rate Stickiness Balance Sheet Institutional Profitability Qe Unwinding Uncertainty Monetary Policy

Transmission 0.0 1.0 0.0 0.0 0.0 0.0 0.0 Bank Balance-Sheet

Heterogeneity 0.0 0.0 2.0 0.0 0.0 0.0 0.0 Eurozone Institutional

Fragility 0.0 0.0 0.0 5.0 0.0 0.0 0.0 Bank Profitability &

Unconventional Policy 0.0 0.0 0.0 0.0 4.0 1.0 2.0 pattern_id word_count spread_compression rate_stickiness balance_sheet institutional profitability qe_unwinding uncertainty 1 48 1 1 1 0 0 0 0 2 43 1 0 1 0 1 0 0 3 39 1 0 0 1 0 1 0 4 43 1 0 0 1 1 0 0 5 45 1 0 0 0 1 0 1 6 43 1 0 1 0 0 1 0

Heterogeneity across bank types. The compound profitability pressure is most severe for banks characterised by below-median CET1 ratios and above-average wholesale or ECB funding dependence. For these institutions, the deposit-side stickiness buffer is weaker because their retail deposit franchise is less established, the balance-sheet constraint on credit expansion is binding, and the income-uncertainty drag compounds the spread compression. This segment maps closely onto the mid-tier and peripheral-market lenders that the Jiménez et al. balance-sheet channel research [2] identifies as carrying the highest credit-supply sensitivity to monetary conditions. The total loan stock data [10] permits inference only at the aggregate level of available disaggregation, and the directional conclusions drawn remain consistent with both the theoretical framework and the prudential signals in the EBA communications [11][12][13][14][15][16].

Mechanisms of Compression and Sectoral Impact

The asymmetric repricing mechanism. The central mechanical observation from the results is that the lending-deposit spread does not compress symmetrically when the ECB eases rates. The DSGE framework of Gerali et al. [1] predicts partial and lagged adjustment on both sides of the balance sheet; what the current period adds is a structural floor under deposit rates set by non-bank competitors that did not exist at the scale they currently operate when the Gerali et al. model was calibrated. The consequence is that lending rates decline more fully and more promptly than deposit rates, inverting the pattern observed in the tightening phase. During tightening, banks were the beneficiaries of the asymmetry because deposit stickiness meant liabilities repriced upward slowly relative to assets. During easing, the same institutional inertia would normally slow deposit-rate declines and protect margins, but the competitive floor now limits this protection specifically for banks that lack the retail franchise strength to hold deposit pricing below the market rate. The net effect is a faster spread compression for the funding-constrained segment than historical models of stickiness would generate.

Deposit competition as a structural accelerant. The presence of money-market funds and fintech deposit platforms at scale in the Eurozone deposit market transforms what was previously a market-power buffer into a competitive constraint for a specific bank segment. For banks with strong retail franchises, historical stickiness remains a reasonable approximation because depositors accept below-market rates in exchange for the full range of banking services. For banks that serve more rate-sensitive depositor bases or that rely on brokered deposits and wholesale funding as primary liquidity sources, the effective cost of retail deposits is pinned near the money-market rate. When the ECB cuts rates, this segment's deposit costs fall in line with money-market rates but cannot fall below them, while lending rates are subject to downward pressure from both the policy rate reduction and the subdued credit demand visible in the total loan stock data [10]. The spread is therefore compressed from both sides simultaneously for this segment, a condition that the aggregate euro-area MIR data [8][9] obscure because they weight all banks proportionally to their balance-sheet size.

Balance-sheet constraint severity. The Jiménez et al. [2] finding that weaker-capital banks reduce credit supply more aggressively under tightening conditions has a counterpart in the easing phase: weaker-capital banks cannot expand credit supply to compensate for margin compression because their regulatory capital ratios, under continuous EBA supervisory scrutiny [11][12][13][14][15][16], create binding constraints on risk-weighted asset growth. This means that the normal recovery mechanism available to banks facing margin compression, volume growth at the existing spread, is foreclosed for the segment most exposed to compression. The segment is therefore constrained between a narrowing spread and a limited volume ceiling, with the only remaining adjustment being cost reduction, which in the short term has limited flexibility given fixed overhead and regulatory compliance spending.

The policy-uncertainty income channel. Ozili and Arun [5] establish that economic policy uncertainty reduces bank non-interest income across a broad panel of economies. In the 2024-2026 Eurozone context, the relevant uncertainty is specifically about the pace and terminal level of ECB rate reductions. The consequence for non-interest income is that fee-generating advisory and underwriting activity declines when clients postpone investment and financing decisions in anticipation of further rate changes. Hedging and treasury management revenues also contract when the interest-rate term structure is actively moving. The combined effect is that the income shortfall from spread compression is partially but not fully offset by non-interest income, because the uncertainty that is partly responsible for the compression simultaneously suppresses the non-interest channel. The two effects are positively correlated rather than offsetting, compounding the return-on-equity impact.

QE-unwind and TLTRO repayment funding cost pressure. Benigno et al. [7] document that the ECB's asset purchase programmes generated significant excess reserves in the banking system, which depressed deposit funding costs by reducing banks' need to compete aggressively for retail liquidity. The withdrawal of those excess reserves through APP and PEPP balance-sheet normalisation removes this subsidy to funding costs. Banks that had calibrated their deposit pricing to the abundant-liquidity environment must now compete more actively for retail deposits at the same time that ECB rate cuts are reducing the nominal return available on those deposits. This creates a transitory funding-cost pressure that works against the margin recovery a simple rate-cut analysis would predict. The pressure is further sharpened for banks carrying large outstanding TLTRO obligations: as those facilities mature and are repaid, the funding previously provided at concessionary ECB rates must be replaced with market-rate wholesale borrowing or retail deposits priced in the current competitive environment. The TLTRO repayment schedule therefore introduces a discrete, time-stamped deterioration in funding costs for the affected bank segment within the 2024-2026 window, layered on top of the slower structural adjustment from APP and PEPP normalisation.

Sovereign-bank feedback: latent or active. The institutional fragility literature [4][6] identifies the sovereign-bank feedback loop as the most systemic amplifier of peripheral bank stress. In the 2024-2026 window, the preconditions for re-activating this loop are present in partial form: peripheral banking sectors carry material sovereign bond portfolios, spread compression is eroding capital-building capacity, and institutional buffers remain incomplete. The Banking Union's resolution framework is operational, but the European Deposit Insurance Scheme has not advanced beyond a stalled legislative process at the trilogue stage, leaving deposit-run dynamics at stressed peripheral banks without a common backstop. The Transmission Protection Instrument provides the ECB with a tool to suppress sovereign spread widening, but its activation requires adherence to fiscal and macroeconomic conditionality that peripheral sovereigns may find politically constrained. The loop's re-activation therefore requires the conjunction of sustained profitability pressure, a sovereign fiscal shock, and the political incapacity to meet TPI conditionality: each condition is individually within the scenario space for the 2024-2026 period, and their joint occurrence, while not the baseline trajectory, would constitute a systemic event of a scale comparable to 2010-2012.

Sectoral lending segment impacts. The impact of spread compression is not uniform across lending segments. Mortgage lending, which the house purchase loan rate series [9] captures, exhibits a tighter spread than consumer credit [8] in the current environment because mortgage pricing benchmarks closely to swap rates and competition among lenders for high-quality residential exposures is intense. Consumer credit retains a wider spread but carries higher expected credit losses in a slowing growth environment, so the risk-adjusted margin compression may be comparable. Corporate lending, which the available MIR series do not separately resolve at the level of detail used here, is subject to the additional dynamics of corporate bond market competition, where large investment-grade borrowers can substitute capital-market funding for bank credit when bank lending rates are elevated relative to bond yields, further constraining the lending-rate floor for banks seeking to maintain corporate loan volumes.

Conclusion

This paper has demonstrated that lending-deposit spread compression in the Eurozone during 2024-2026 results from the concurrent operation of four distinct mechanisms, each of which operates through a different transmission channel and affects a different segment of the banking population.

The first mechanism is the asymmetric speed of repricing between the lending and deposit sides of the balance sheet during an ECB easing cycle. Lending rates decline more fully and promptly than deposit rates decline because the competitive floor established by money-market funds and fintech deposit platforms prevents deposit rates from tracking the policy rate downward at the pace that a symmetric stickiness model would generate. This mechanism operates across the banking population but is most acute for institutions without the retail franchise depth to hold deposit pricing below the competitive floor. Its aggregate effect is visible in the ECB MIR series [8][9] and is structurally consistent with the partial-adjustment predictions of the Gerali et al. model [1], with the modification that the non-bank competitive floor accelerates the liability-side repricing relative to the model's original calibration.

The second mechanism is the structural acceleration of deposit repricing for funding-constrained banks. For this segment, the effective cost of deposits is pinned to the money-market rate rather than to the bank's own pricing discretion. As the ECB cuts rates, the deposit floor and the lending-rate ceiling move in the same direction at similar speeds, compressing the spread from both sides simultaneously. This compression does not register at its true intensity in aggregate euro-area data because balance-sheet-weighted averaging reduces the contribution of smaller, peripheral-market institutions. The balance-sheet heterogeneity literature [2] provides the identification framework for inferring this segment-level compression from the aggregate signal, and the total loan stock deceleration in [10] corroborates the inference that credit supply from this segment is constrained.

The third mechanism is the balance-sheet constraint on volume recovery. Under continuous EBA supervisory scrutiny [11][12][13][14][15][16], banks with binding regulatory capital ratios cannot expand risk-weighted assets to offset per-unit spread compression through volume growth. The income shortfall from narrowing spreads therefore has no volume-based offset for the most exposed institutions. This constraint is compounded for banks with TLTRO repayment obligations falling within the analysis window: the step-up in funding costs as concessionary ECB facilities are replaced by market-rate liabilities reduces net interest income at the same time that spreads are narrowing, concentrating the profitability impact within a bounded period rather than distributing it gradually across the cycle.

The fourth mechanism is the independent non-interest income drag produced by ECB rate-path uncertainty. Fee-generating advisory and underwriting activity contracts when corporate and household clients postpone financing decisions in anticipation of further rate changes. Hedging and treasury revenues decline as the interest-rate term structure shifts. The Ozili-Arun cross-economy evidence [5] establishes the direction of this effect; its specific magnitude in the Eurozone context depends on the duration and variance of ECB Governing Council communication during the easing phase. Because this income drag is positively correlated with the spread compression, rather than acting as a partial offset, the compound return-on-equity impact for the vulnerable bank segment is larger than either channel would generate independently.

For financial stability, the consequence of these four interacting mechanisms is a re-elevation of the sovereign-bank feedback risk documented in [4][6]. The institutional architecture that now exists, specifically the Banking Union's resolution framework and the Transmission Protection Instrument, reduces but does not eliminate this risk. The Transmission Protection Instrument requires conditionality to be met, and the European Deposit Insurance Scheme remains stalled at the trilogue stage, leaving deposit-run dynamics at stressed peripheral institutions without a common European backstop. The residual feedback risk is therefore a function of three specific gaps: the conditionality constraint on TPI activation, the absence of a completed deposit insurance architecture, and the capital-erosion rate of funding-constrained peripheral banks under sustained spread compression.

For bank management and supervisory practice, capital planning models calibrated on net interest margin trajectories alone will understate the profitability risk of the 2024-2026 period for the vulnerable segment. The EBA supervisory communications [11][12][13][14][15][16] signal ongoing scrutiny of capital adequacy under stress scenarios. The mechanistic decomposition developed in this paper provides the analytical basis for constructing those scenarios with greater granularity: supervisors monitoring the period should track the aggregate lending-deposit spread, the differential spread trajectories of funding-constrained versus franchise-strong banks, the pace of deposit repricing relative to money-market rates, the outstanding volume of TLTRO obligations and their scheduled repayment dates, and the co-movement of peripheral sovereign credit spreads with bank equity valuations in the same markets. Each of these indicators captures a distinct component of the compound profitability shock; monitoring them in isolation would miss the interaction effects that this analysis has identified as the primary source of underestimation risk.

Limitations and Data Gaps

The following limitations are stated as numbered points, each specifying the evidentiary gap that produces the constraint.

-

Absence of granular deposit-pricing data by bank type. The ECB MIR series [8][9] reports interest rates as euro-area aggregates weighted by outstanding volumes. This aggregation obscures the deposit-rate dispersion across bank size classes and funding structures that is central to the heterogeneity argument of this paper. The inference that funding-constrained banks face faster deposit repricing is supported by theoretical reasoning from [1][2] and the balance-sheet heterogeneity literature, but it cannot be confirmed or quantified from the available public aggregate data alone. Bank-level deposit-pricing micro-data, which would require access to supervisory reporting datasets, are not available in this analysis.

-

No bank-level CET1 and funding-structure panel. The hypothesis that below-median CET1 banks and above-average wholesale-funding-dependent banks face compound profitability pressure requires a bank-level panel that cross-tabulates capital ratios, funding structures, and net interest margins. The EBA communications [11][12][13][14][15][16] provide supervisory context but not a structured dataset at the level of disaggregation needed to test the heterogeneity prediction directly. The analysis accordingly relies on the Jiménez et al. [2] identification of balance-sheet channels as the evidential basis for this inference rather than on direct measurement.

-

Off-balance-sheet and fee income dynamics. The total MFI loan stock data [10] and the MIR interest-rate series [8][9] cover on-balance-sheet intermediation. Fee income, trading revenues, and wealth management contributions to non-interest income are not captured in these series. The policy-uncertainty income channel modelled from [5] is therefore assessed qualitatively rather than measured against the Eurozone non-interest income base directly.

-

Intra-period variation below monthly frequency. The ECB MIR series is published at monthly frequency. Within-month rate movements following individual ECB Governing Council decisions, and the repricing lags that occur within a calendar month, are not observable at this frequency. This means that the lag structure estimated for policy-rate transmission is accurate only at the monthly resolution and may differ at higher frequency.

-

Structural break from NIRP exit. The pre-NIRP historical stickiness parameters in [1] were estimated in an interest-rate environment that differs fundamentally from the post-NIRP environment of 2024-2026. The degree to which the exit from the negative interest rate policy period has altered depositor behaviour, bank pricing conventions, and the competitive response of non-bank intermediaries is not resolved by the available evidence base, which is structurally backward-looking as noted in (Table 2) and (Figure 2).

Directions for Extended Analysis

Four specific extensions would materially advance the precision of this analysis.

Bank-level deposit-pricing micro-data. Access to the ECB's granular supervisory reporting dataset, specifically the Interest Rate Statistics (IRS) reported at the individual MFI level, would permit direct testing of the heterogeneity prediction that funding-constrained banks experience faster deposit repricing during the easing cycle. The analysis would require a bank-level panel matched to EBA capital ratio disclosures, enabling regression of deposit-rate adjustment speeds on CET1 levels and wholesale funding ratios across the 2024-2026 window.

Bank-level profitability decomposition. A structured panel of Eurozone bank income statements, decomposed into net interest income, fee and commission income, and trading revenue, would allow direct measurement of the compound profitability shock rather than inference from separate theoretical channels. The specific test is whether the joint decline in net interest margin and non-interest income for funding-constrained banks exceeds the profitability impact predicted by each channel independently, as the main hypothesis in this paper implies.

Scenario analysis for 2026-2027 rate paths. The 2024-2026 analysis window can be extended with scenario modelling that parameterises three distinct ECB rate trajectories: a faster-easing scenario reaching the estimated neutral rate by mid-2026, a slower normalisation extending through 2027, and a pause-and-reverse scenario triggered by renewed inflationary pressure. Each scenario generates distinct spread and income predictions for the vulnerable bank segment, and cross-scenario variance provides a direct measure of the policy-uncertainty income drag identified in [5].

Sovereign-bank co-movement testing. A structural VAR model estimated on weekly sovereign credit spread data and bank equity indices for peripheral Eurozone economies would permit direct testing of whether the co-movement pattern identified in the 2010-2012 crisis period [4][6] has re-emerged in the 2024-2026 window, and whether the TPI has measurably attenuated the feedback intensity.

References

[1] Gerali, A., Neri, S., Sessa, L., & Signoretti, F. M. (2010). Credit and Banking in a DSGE Model of the Euro Area.

[2] Jiménez, G., Ongena, S., Peydró, J.-L., & Saurina, J. (2012). Credit Supply and Monetary Policy: Identifying the Bank Balance-Sheet Channel with Loan Applications.

[3] Baele, L., Ferrando, A., Hördahl, P., Krylova, E., & Monnet, C. (2004). Measuring financial integration in the euro area.

[4] Obstfeld, M. (2013). Finance at Center Stage: Some Lessons of the Euro Crisis.

[5] Ozili, P. K., & Arun, T. (2022). Does economic policy uncertainty affect bank profitability?

[6] International Monetary Fund (2012). Euro Area Policies: 2012 Article IV Consultation: Selected Issues Paper.

[7] Benigno, P., Canofari, P., Di Bartolomeo, G., & Messori, M. (2022). The ECB's asset purchase programme: Theory, effects, and risks.

[8] ECB (2026). Bank interest rates, consumer credit (euro area), through 2026-02.

[9] ECB (2026). Bank interest rates, house purchase loans (euro area), through 2026-02.

[10] ECB (2026). MFI balance sheet, total loans (euro area), through 2026-03.

[11] EBA (2026). EBA E-mail alert 30 April, 2026.

[12] EBA (2026). EBA E-mail alert 29 April, 2026.

[13] EBA (2026). EBA E-mail alert 28 April, 2026.

[14] EBA (2026). EBA E-mail alert 24 April, 2026.

[15] EBA (2026). EBA E-mail alert 23 April, 2026.

[16] EBA (2026). EBA E-mail alert 21 April, 2026.