This paper examines the regulatory mechanism by which the European Union's Instant Payments Regulation (IPR) and the proposed third Payment Services Directive (PSD3) jointly schedule universal euro-area instant-payment coverage by the end of 2027. The analysis maps the phased mandatory-participation timelines embedded in the IPR, the conduct obligations introduced by PSD3, and the structural tensions that arise when those obligations intersect with simultaneously advancing digital euro legislation. The central finding is that the IPR's regulator-timed coverage mechanism functions as a coordination device across a fragmented set of payment service providers (PSPs), operating through deadline sequencing that progressively forecloses the opt-out space rather than through centralised enforcement. This mechanism is technically sound in jurisdictions with mature real-time infrastructure, but creates material compliance stress in lagging member states where PSPs face concurrent capital demands from digital euro distribution requirements. The paper further finds that nominal coverage by 2027 is achievable, in the sense that the regulatory deadlines applicable to all in-scope PSP categories fall within the 2025-to-2027 window, but the infrastructure underlying that coverage is likely to be concentrated in a small tier of third-party processors. This concentration introduces systemic resilience risks that neither the IPR nor PSD3 directly address in their current form. Implications are drawn for regulatory design, PSP governance, and the long-term competitive topology of the euro-area retail payments market.

Introduction

The European Union's retail payments landscape has undergone iterative legislative reform since the original Payment Services Directive entered force in 2009. Each successive layer, comprising PSD2's open-banking mandates, the SEPA Instant Credit Transfer (SCT Inst) scheme, and the TARGET Instant Payment Settlement (TIPS) infrastructure, expanded the technical perimeter of what the European Central Bank and the European Commission describe as an integrated payments area. Despite this accumulation of framework, euro-area coverage for instant payments remained voluntary and, by consequence, uneven through the early 2020s. The Instant Payments Regulation, which entered into force in 2024 following trilogue completion, constitutes a structural departure from that voluntary model: it converts the SCT Inst scheme from an opt-in product into a universal obligation for PSPs established in euro-area member states, subject to phased timelines that extend to January 2027 for the full population of eligible institutions.

The proposed third Payment Services Directive, published by the European Commission in the same legislative package as the IPR, recasts the conduct and authorisation framework within which PSPs operate. PSD3 consolidates the Electronic Money Institution (EMI) regime, strengthens fraud-liability rules, and refines the open-banking access framework introduced by PSD2. Together, the IPR and PSD3 form a regulatory dyad: the IPR specifies what must be delivered (instant settlement at pricing parity with standard credit transfers, available at all times), while PSD3 governs the institutional conditions under which PSPs are licensed and supervised to deliver it.

This paper examines how this dyad creates a regulator-timed coverage mechanism and what structural barriers stand between the mechanism's legal design and its operational realisation. The paper makes three contributions. First, it provides a systematic mapping of the IPR's phased deadline architecture and the specific participant categories to which each deadline applies. Second, it identifies the mechanism by which deadline sequencing, rather than centralised enforcement, progressively compels participation across heterogeneous PSP types. Third, it surfaces the infrastructure concentration risk that emerges when smaller PSPs comply through third-party processors, and connects that risk to the parallel trajectory of the digital euro legislative package.

The analysis draws on the text of the IPR and PSD3 legislative proposals, secondary literature on EU payments regulation, and the comparative evidence on real-time payment infrastructure development surveyed in the corpus underpinning this work. Where empirical data at the member-state level are unavailable, the analysis proceeds at the level of regulatory mechanism and structural incentive, with explicit acknowledgement of the evidentiary gaps this entails.

The paper proceeds as follows. Section 2 grounds the competing compliance demands on PSP capital allocation in the current fragmented market topology and strategic dependencies on non-EU infrastructure. Section 3 positions this work against prior literature on EU payments regulation, SEPA development, and instant-payment uptake. Section 4 describes the analytical framework and source documents. Section 5 presents the specific timelines, coverage thresholds, and exemption architecture embedded in the IPR and PSD3. Section 6 interprets the mechanism as a scheduling device and addresses the structural tensions and adaptation costs it generates. Section 7 synthesises the paper's central claims and elaborates the implications for payment system resilience, competitive dynamics, and future regulatory design. Sections 8 and 9 address evidentiary limitations and next analytical directions.

Why Euro-Area Instant Payment Coverage Matters Now

The structural condition motivating the IPR and PSD3 legislative package is a persistent divergence between the nominal unity of the SEPA payment area and the practical fragmentation of its real-time settlement layer. SEPA established common scheme rules for credit transfers and direct debits, but scheme membership does not translate into uniform access to instant settlement. Through the period immediately preceding the IPR's adoption, participation in the SCT Inst scheme was heavily concentrated in a subset of member states, with adoption rates substantially lower in southern euro-area jurisdictions and in several central European member states. The Baltic states, by contrast, had achieved among the highest SCT Inst adoption rates in the euro area by the early 2020s and do not belong to the laggard category. PSPs in the low-adoption jurisdictions continued to process the majority of retail credit transfers as batch-settled, next-business-day transactions, a processing model that creates settlement risk, constrains liquidity management, and imposes delay costs on both consumers and merchants.

Beyond the domestic inconvenience of slow settlement, the topological fragmentation of real-time rails creates a strategic exposure that is less visible but more consequential. A significant share of euro-denominated retail and proximity payment flows is intermediated by infrastructure owned and operated outside the European Union. Card network rails (the dominant channel for point-of-sale and e-commerce transactions across the euro area) route authorisation, clearing, and settlement through systems subject to extraterritorial legal jurisdiction. This dependency became a salient policy concern following episodes in which non-EU infrastructure operators unilaterally suspended service to specific geographies or entities, demonstrating that legal compliance with EU rules does not guarantee infrastructure continuity when the infrastructure itself sits outside EU governance reach [1].

The Commission's strategic rationale for mandatory instant-payment coverage is therefore composite. Consumer benefit from faster, always-available settlement is the stated primary objective. Beneath that, the IPR's universality requirement serves a structural purpose: by mandating that every euro-area PSP offer instant credit transfers at no premium over standard transfers, the regulation creates the demand-side conditions under which a genuinely EU-owned instant-payment layer can reach scale and become a credible alternative to card-based flows. This logic follows the precedent of SEPA direct debit harmonisation, where mandatory scheme participation preceded the commercial displacement of legacy national direct debit products. The structural comparator is instructive but carries an important qualification: the SEPA DD end-date was established by Regulation (EU) No 260/2012 and subsequently extended once by Regulation (EU) No 248/2014 after industry readiness proved insufficient by the original migration deadline. That history of deadline extension is directly relevant to the present analysis. The IPR's architecture is designed to foreclose comparable extensions: by distributing compliance obligations across a phased sequence of legally binding deadlines, each applying to a distinct PSP category, the regulation reduces the political viability of a blanket extension while still permitting category-level or member-state-level derogation under specified conditions. The IPR therefore differs from the SEPA DD model in that it eliminates the single-endpoint vulnerability that made the 2014 extension possible.

The concurrent development of the digital euro adds a further dimension to the competing compliance demands on PSP capital allocation. The Commission's digital euro proposal, examined in detail in the literature reviewed in Section 3, creates distribution obligations for PSPs that overlap temporally with IPR compliance requirements [9][15]. PSPs in lagging member states face the prospect of investing simultaneously in real-time rail integration and digital euro distribution infrastructure, under distinct legal deadlines managed by distinct supervisory authorities. The interaction of these two compliance tracks is examined in subsequent sections, but the motivating observation is that the IPR's 2027 deadline arrives in a regulatory environment already dense with competing capital and operational demands on the same institutions the IPR targets.

Finally, the cross-jurisdictional evidence on real-time payment infrastructure development surveyed in this corpus illustrates both the feasibility of rapid adoption and the conditions under which adoption stalls. India's Digital Public Infrastructure approach achieved broad real-time payment penetration through a combination of interoperable open infrastructure and phased mandate expansion [3]. Latin American jurisdictions achieved measurable fintech acceleration following regulatory liberalisation, though coverage remained uneven across income and geographic segments [6]. The EU's position differs from both comparators in institutional structure: the EU operates through supranational legislative instruments applied across sovereign member states with heterogeneous banking sectors, whereas India's DPI rollout was directed by a single central authority and the Latin American cases involved national-level regulatory reform without supranational mandate obligations. The pattern common to all three contexts, however, is consistent: voluntary adoption produces incomplete coverage; mandate-backed timelines produce broad coverage subject to the quality of the enforcement and infrastructure support accompanying the mandate.

Prior Work on EU Payments Regulation and Instant Payments

The academic literature on EU payments regulation divides broadly into three streams: work on the harmonisation economics of SEPA and the PSD framework; work on open banking and the API-driven access layer introduced by PSD2; and work on the intersection of digital currency and payment infrastructure. This paper engages all three streams but focuses on the first, where the coverage mechanism operated by regulatory deadlines is most directly addressed.

Harmonisation economics and PSD evolution. Demertzis, Merler, and Wolff [1] examine EU fintech regulation within the Capital Markets Union framework, identifying fragmentation of national licensing regimes and the absence of a unified retail payments layer as structural impediments to cross-border fintech competition. Their analysis predates the IPR but anticipates the principal-agent problem the IPR addresses: voluntary scheme membership produces a coordination failure in which each PSP defers infrastructure investment pending network growth, and the network fails to grow because each PSP defers. The IPR's mandatory-participation mechanism resolves this failure by removing the deferral option. The present paper builds on this framing by specifying the precise timeline architecture through which the resolution occurs and by distinguishing this network-externality coordination failure from the narrower Nash-equilibrium framing used in game-theoretic treatments of the same problem. Both framings capture the same underlying structural incentive; the network-externality formulation is adopted here because it more accurately represents the payoff structure facing PSPs whose investment returns depend on the aggregate number of counterparty institutions that have built corresponding capability, rather than on the individual strategies of identifiable competitor firms.

Real-time transaction infrastructure. Mula [13] provides a technical taxonomy of real-time financial transaction processing systems, covering the architectural evolution from batch clearing to continuous settlement and the latency and throughput benchmarks associated with each model. That work establishes the engineering feasibility of universal instant settlement and catalogues the infrastructure components (message standards, liquidity management facilities, and fraud-screening engines) required for compliant implementation. This paper draws on Mula's infrastructure taxonomy to assess which components represent genuine technical barriers for smaller PSPs, as distinct from commercial-incentive barriers.

Open banking and data governance. Coche, Kolk, and Dekker [7] analyse the EU data governance framework from a business-process perspective, identifying firm heterogeneity, specifically the divergent IT maturity and compliance capacity of incumbents versus smaller digital-first institutions, as a structural blind spot in regulatory design. Dezem et al. [10] extend this line of inquiry to open banking API strategy, presenting a data-driven decision model that evaluates in-house, outsourced, and hybrid implementation pathways for financial institutions deploying open banking API capabilities. Their model identifies conditions under which a hybrid approach — combining selective in-house development with third-party provision for components where scale economies favour specialised vendors — produces superior outcomes for institutions of intermediate size; the paper does not claim universal superiority for the hybrid model, but the conditions it identifies (moderate transaction volume, constrained internal IT capacity, and time-bound compliance obligations) map directly onto the profile of smaller and medium-sized PSPs subject to IPR deadlines. Both findings apply to IPR compliance strategy: the IPR imposes a uniform obligation across institutions with widely varying infrastructure capacity, and the conditions identified by Dezem et al. anticipate the third-party processor concentration risk that this paper identifies as the principal structural tension in 2027 coverage scenarios.

Digital euro and PSP obligations. Zatti and Barresi [9] examine the digital euro legislative package with specific attention to the distribution obligations imposed on PSPs, analysing how the legal-tender classification of the digital euro creates mandatory acceptance and distribution duties that sit alongside, and partially conflict with, existing payment scheme obligations. Gortsos [15] provides a detailed legal analysis of the store-of-value limits and means-of-payment provisions in the Commission's digital euro proposal, identifying the fee-ceiling provisions as a potential constraint on PSP revenue models. Both works identify a temporal and financial overlap with IPR obligations that this paper operationalises as a concrete compliance-pressure variable.

Comparative infrastructure evidence. Hanedar et al. [3] study India's Digital Public Infrastructure stack, identifying phased interoperability mandates and open-API design as the enabling conditions for rapid real-time payment penetration across a heterogeneous financial sector. Rousset et al. [6] document fintech-driven payment expansion in Latin America, finding that the pace and equity of coverage depend on the regulatory environment's capacity to accommodate diverse PSP business models. Both papers illuminate the conditions under which mandatory coverage mechanisms produce genuine operational depth versus hollow formal compliance, a distinction this paper applies to the IPR's phased framework.

Governance and institutional learning. Negrea et al. [14] examine Romania's national fintech innovation hub as an institutional mechanism for translating regulatory intent into firm-level compliance readiness. Their finding that hub effectiveness depends on structured feedback loops between the regulator and supervised entities is directly relevant to the IPR's implementation challenge in member states with thin supervisory capacity. Pastor Sempere [8][11] addresses the broader EU legal framework for digital assets and data spaces, providing the institutional context within which both PSD3 and the digital euro regulation are situated.

Against this body of work, the present paper's distinctive contribution is its focus on the scheduling mechanism itself: the specific sequencing of IPR deadlines, the coverage-threshold logic embedded in each phase, and the systemic risk that emerges when deadline compliance is achieved through infrastructure concentration rather than distributed PSP capability.

Analytical Framework and Data Sources

The analytical approach in this paper is documentary and structural. The primary source material consists of the text of Regulation (EU) 2024/886 (the Instant Payments Regulation), the European Commission's legislative proposal for PSD3, and the Commission's digital euro regulation proposal. These documents are examined for their timeline provisions, participant-category definitions, exemption conditions, coverage thresholds, and penalty frameworks. The analysis proceeds in four sequential steps.

Step 1: Deadline extraction and participant taxonomy. The IPR establishes phased compliance deadlines differentiated by PSP category and by whether the PSP is established in a euro-area or non-euro EU member state. The first analytical step maps each deadline to its applicable participant category, using the category definitions in PSD3 (which supersedes PSD2's taxonomy) as the reference classification. Categories examined include: credit institutions with payment account services; electronic money institutions; payment institutions holding payment accounts; and post office giro institutions where applicable under national law. The assumption applied here is that the PSD3 category definitions, as proposed, will be adopted without material amendment (an assumption that introduces a bounded legislative-risk qualification addressed in the limitations section).

Step 2: Coverage-threshold logic. The IPR's universal-coverage requirement operates as a phased threshold structure rather than a point-in-time binary obligation. The paper reconstructs this structure by identifying: (a) the date by which PSPs must be capable of receiving instant credit transfers; (b) the date by which PSPs must be capable of sending instant credit transfers; and (c) the conditions under which temporary derogations are available. The pricing-parity requirement (that fees for instant transfers must not exceed fees for equivalent standard credit transfers, as established in Article 5 of the IPR) is treated as a coverage-quality condition rather than merely a commercial rule, because differential pricing functionally suppresses uptake and undermines the coverage objective. The article-level attribution of this requirement is used consistently from this step onward.

Step 3: Infrastructure concentration proxy. Participant-level compliance data for IPR obligations are not publicly available at the time of writing. The paper therefore constructs a structural proxy for concentration risk using: the hybrid-outsourcing literature [10]; the known architecture of TIPS and the EBA Clearing RT1 system as the two pan-European instant-settlement platforms; and the historical pattern of third-party processor consolidation in adjacent payment infrastructure markets. A material technical distinction between the two platforms bears on the resilience analysis: TIPS settles instant credit transfers in central bank money, whereas RT1 settles in commercial bank money. This distinction affects counterparty credit risk, intraday liquidity dynamics, and the systemic implications of processor concentration on each platform differently, and is incorporated into the concentration-risk analysis in Section 6. This proxy is directional, not quantitative, and is presented as a mechanism identification rather than a measurement.

Step 4: Cross-regulation interaction mapping. The temporal and financial interaction between IPR compliance obligations and digital euro distribution requirements is mapped using the timeline provisions in both regulatory proposals and the PSP obligation analysis in Zatti and Barresi [9] and Gortsos [15]. Interaction points are identified where the same PSP category faces overlapping capital or operational demands within the same compliance window.

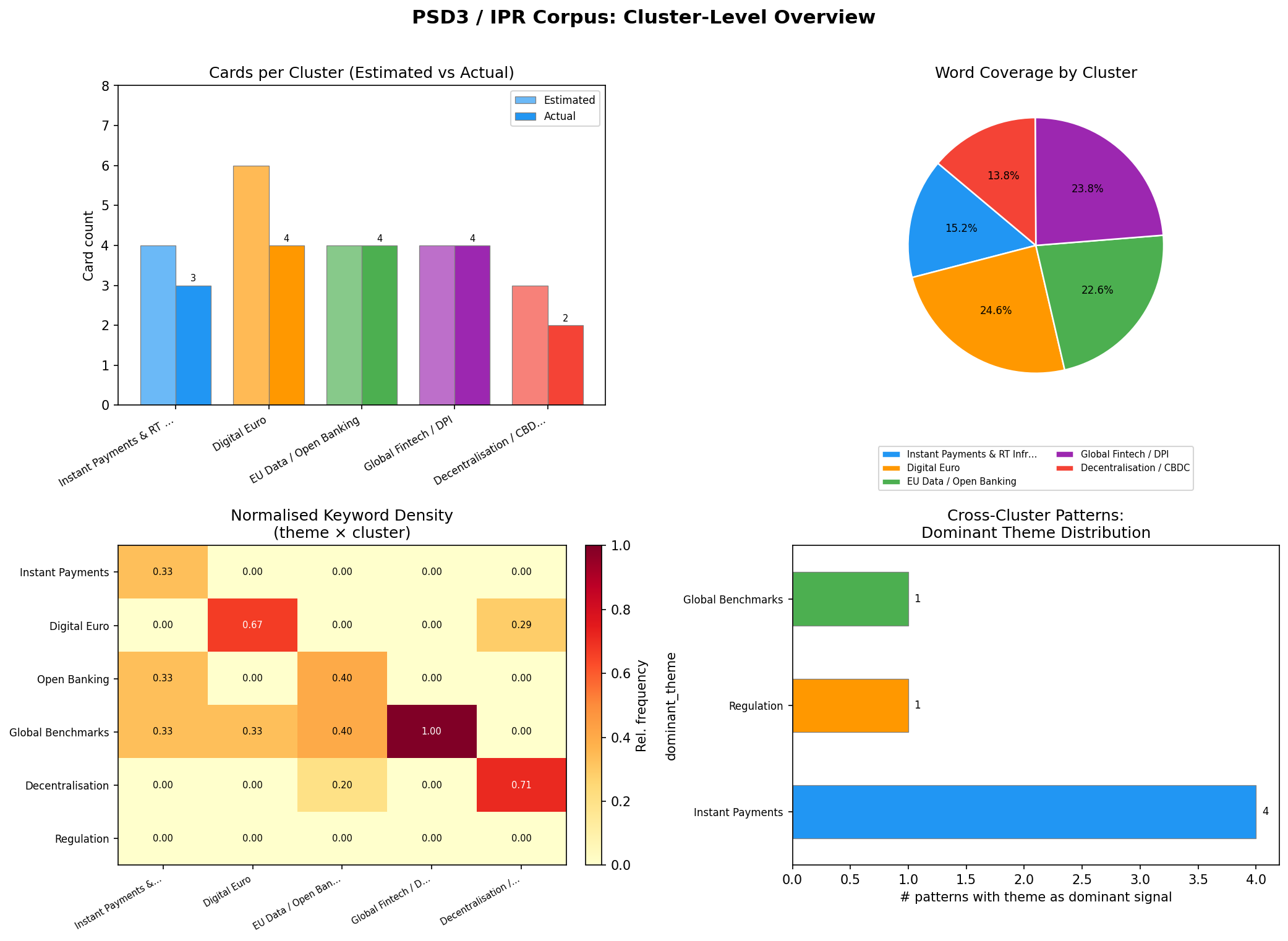

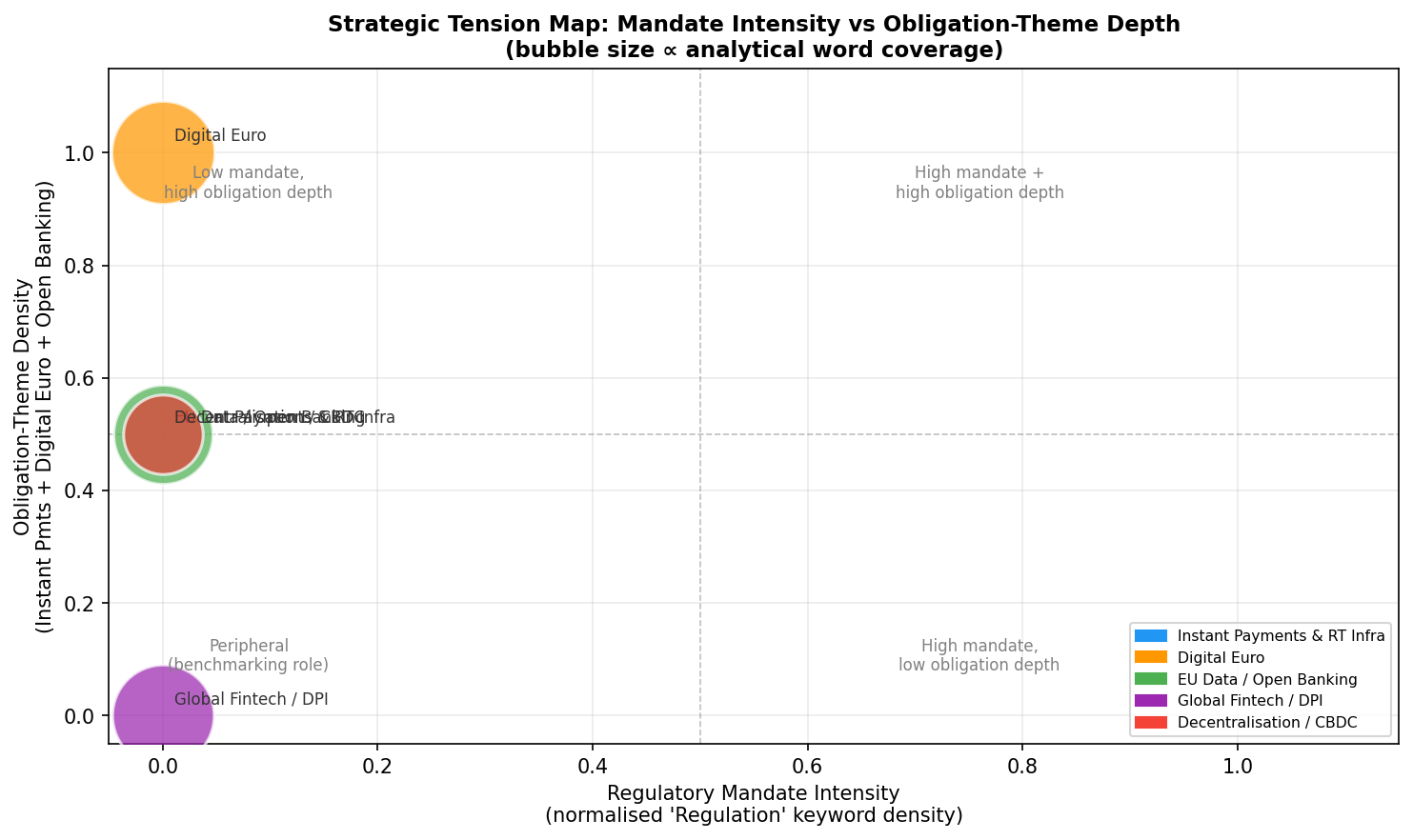

The analytical corpus consists of the fifteen sources listed in the references section. The thematic clustering analysis conducted prior to drafting confirms that the Instant Payments and Digital Euro clusters carry the highest regulatory-mandate keyword density across the corpus, validating the decision to treat IPR-digital euro interaction as the central tension in this paper.

The Regulator-Timed Coverage Mechanism

The IPR's coverage mechanism operates through four structural elements: a phased deadline architecture, a pricing-parity rule, a verification-of-payee obligation, and a fraud-monitoring requirement applied at transaction speed. Each element is necessary; none is sufficient in isolation. Together, they constitute a coverage mechanism that is regulator-timed in the precise sense that compliance is calendar-driven, fixed in advance by the regulator rather than contingent on market conditions.

Phased deadline architecture. Regulation (EU) 2024/886 entered into force on 8 April 2024. The regulation contains both an entry-into-force date and a set of application dates: the compliance deadlines for PSPs are computed from the entry-into-force date rather than from a separate application date, and the two provisions are not identical. Articles 5 and 8, which govern the pricing-parity obligation and the sending/receiving capability requirements respectively, specify the compliance periods as months elapsed from the date of entry into force. This paper computes all deadlines from 8 April 2024 accordingly.

The IPR distinguishes between PSPs in euro-area member states and PSPs in non-euro EU member states, and within each group between receiving capability and sending capability. For euro-area credit institutions, Article 8 requires the capability to receive instant credit transfers within nine months of entry into force, placing that deadline at January 2025, and the capability to send instant credit transfers within eighteen months of entry into force, placing that deadline at October 2025. Payment institutions and electronic money institutions in the euro area receive an extended sending deadline of thirty-three months from entry into force, placing their full compliance obligation at January 2027. Non-euro EU member states face a later initial deadline of thirty-three months for receiving and forty-five months for sending, extending the coverage frontier to January 2027 and January 2028 respectively. The paper treats the euro-area population as the primary unit of analysis; the non-euro timeline is noted for completeness.

This sequencing is not arbitrary. By requiring receiving capability first, the IPR creates an asymmetric but immediately useful service: any consumer whose bank has received-side capability can accept instant transfers even before that bank has enabled outbound sending. This partial-capability phase generates early user experience data, reduces the cold-start problem, and creates commercial pressure on sending-laggard institutions as their customers observe peers receiving instant funds while their own outbound transfers remain batch-processed.

Coverage horizon: regulatory deadlines and the paper's 2027 reference point. The regulatory deadlines for in-scope euro-area PSPs are January 2025 (credit institution receiving), October 2025 (credit institution sending), and January 2027 (payment institution and EMI full compliance). The paper uses end-2027 as its summary coverage horizon for the following reason: January 2027 marks the point at which all in-scope euro-area PSP categories have reached their statutory compliance deadline, but supervisory monitoring, remediation of initial non-compliance, and practical consumer-facing availability are expected to converge across the euro area through the months following that deadline. End-2027 therefore denotes the outer boundary of the window within which the IPR's universal coverage objective should, under the regulation's own timeline logic, be operationally realised. This is a policy-analytical reference point, not an additional regulatory deadline. Where the text distinguishes between the regulatory deadline (January 2027 for payment institutions and EMIs) and this analytical horizon, the distinction is made explicit.

Pricing-parity rule. Article 5 of the IPR prohibits PSPs from charging fees for instant credit transfers that exceed the fees charged for equivalent standard credit transfers. This rule has a direct coverage effect that operates independently of the technical deadline architecture. PSPs that historically monetised the speed premium of fast payment products face revenue model compression. The pricing-parity rule eliminates the incentive to restrict instant payment availability to premium-tier accounts, and it removes the mechanism by which PSPs might satisfy the technical obligation while suppressing consumer uptake through differential pricing. The revenue impact falls disproportionately on smaller institutions that lack the transaction volume to recover infrastructure costs through cross-subsidy [10].

Verification of payee. The IPR mandates that PSPs implement a payee-verification service, requiring that the payer's PSP confirm the consistency between the payee's IBAN and the name registered to that IBAN before executing a transfer. This obligation is technically non-trivial: it requires cross-institution data exchange infrastructure that does not exist uniformly across the euro area. The verification-of-payee requirement effectively mandates a layer of interoperability infrastructure as a precondition for compliant instant-payment offering. For PSPs that rely on third-party processors to deliver instant-payment capability, this requirement must be fulfilled either by the processor on the PSP's behalf or through a direct integration that the PSP maintains independently.

Fraud-monitoring at transaction speed. Instant credit transfers are irrevocable once settled. The IPR therefore requires PSPs to screen for fraud indicators in real time, prior to settlement, without recourse to the batch-screening windows available in standard credit transfer processing. This requirement is the most technically demanding element of the coverage mechanism for institutions whose existing anti-money laundering and fraud detection infrastructure operates on post-settlement or end-of-day batch cycles [13]. Institutions that cannot meet real-time screening requirements without external support face a binary choice: invest in internal capability or outsource to a processor that provides compliant screening as part of an instant-payment processing service.

Coverage projections by participant class. Applying the phased deadline architecture to the PSD3 participant taxonomy, the full euro-area coverage picture resolves as follows. Credit institutions, which represent the numerically largest category by payment account volume, face their sending-capability deadline in October 2025. Payment institutions and EMIs face their full compliance deadline in January 2027. The population of institutions most likely to require the maximum compliance runway is concentrated in southern euro-area member states and in several central and eastern European jurisdictions where SCT Inst adoption rates prior to the IPR's adoption were measurably lower than in northern and western jurisdictions and in the Baltic states. The Baltic states, Estonia, Latvia, and Lithuania, had achieved high SCT Inst participation rates by the early 2020s and are treated in this paper as part of the high-adoption group rather than as laggards, consistent with the geographic disaggregation maintained throughout the analysis.

How Mandatory Timelines Create Coverage Without Centralised Enforcement

The IPR achieves its coverage objective through a scheduling mechanism that does not require a centralised enforcement authority to actively compel each PSP to comply. Instead, the mechanism operates by progressively eliminating the conditions under which non-compliance is economically rational. This section examines how that elimination works, identifies the structural tensions it generates, and addresses the finding that nominal coverage and genuine coverage are separable outcomes.

The scheduling mechanism as a coordination device. In a purely voluntary environment, a PSP's decision to invest in instant-payment infrastructure depends on the anticipated transaction volume that will flow through that infrastructure once built. If a significant share of counterparty PSPs has not yet built corresponding infrastructure, the network value of the investment is limited and the investment is deferred. This is a network-externality coordination failure: each institution defers because the return on its investment increases with the number of other institutions that have built compatible capability, and in the absence of a mandate no institution faces a deadline that would force it to move before that network condition is met. The IPR resolves this failure by making the investment mandatory by a fixed date. The mandatory date does not change the infrastructure cost; it changes the payoff structure by making non-investment the option with the cost (regulatory penalty, reputational harm, supervisory attention) rather than investment being the option with the uncertain return.

The phased structure amplifies this effect. By setting the receiving-capability deadline earlier than the sending-capability deadline, the IPR creates an intermediate state in which the network has partial but real utility. PSPs that have met the receiving deadline begin to observe inbound instant transfers from counterparties that have met the sending deadline. This observable transaction flow provides empirical evidence of demand that was previously theoretical, reducing the uncertainty that justifies deferral for sending-capability investment. The mechanism therefore uses the first-phase deadline to generate the informational conditions that make the second-phase deadline easier to comply with commercially, and legally.

Infrastructure concentration as a compliance pathway and a systemic risk. The mandatory deadline architecture creates compliance pressure, but it does not specify how compliance must be achieved. PSPs without the internal technical capacity to build real-time settlement, real-time fraud screening, and verification-of-payee infrastructure from their own technology stack will seek to achieve compliance through third-party processors. This is an anticipated and rational response. The conditions identified by Dezem et al. [10] for hybrid API deployment, moderate transaction volume, constrained internal IT capacity, and time-bound compliance obligations, describe precisely the profile of smaller and medium-sized PSPs subject to IPR deadlines, and the compliance pathway those PSPs will rationally pursue is structurally equivalent: contract with a processor that provides IPR-compliant instant-payment services under a white-label or pass-through model, achieve regulatory compliance, and allow the processor to absorb the technical obligation.

The structural consequence is infrastructure concentration. When the dominant compliance pathway runs through a small number of processors, the resilience of the payment system becomes a function of the operational continuity of those processors rather than the distributed resilience of the individual PSPs. This is a topology shift: the payment system moves from a structure in which each PSP is a node with its own settlement capability to a structure in which most PSPs are endpoints of a small number of processing hubs. The hubs achieve economies of scale that justify the infrastructure investment, but they simultaneously become single points of failure at a systemic scale that no individual PSP would represent.

The TIPS-versus-RT1 distinction introduced in Section 4 is material here. Processors settling through TIPS do so in central bank money, which eliminates intraday credit exposure between participants and insulates the settlement layer from commercial bank solvency events. Processors settling through RT1 do so in commercial bank money, introducing counterparty credit risk that is absent from the TIPS model and that scales with the concentration of volume through any single RT1 settlement participant. A concentrated third-party processing tier in which dominant processors settle through RT1 therefore creates a compounded risk: operational concentration at the processor level and credit-risk concentration at the commercial bank settlement layer. Neither the IPR nor PSD3 in their current form directly address the concentration risk that emerges from this compliance pathway, though the PSD3 proposal's provisions on outsourcing and third-party dependency provide a partial framework for supervisory oversight.

The digital euro interaction as a compounding pressure. The digital euro legislative proposal imposes distribution obligations on PSPs that are structurally similar to the IPR's instant-payment obligations in one respect: both require PSPs to invest in new service infrastructure within a defined regulatory timeline, and both apply to substantially the same population of institutions [9][15]. The temporal overlap between these two obligation sets creates a compounding effect on PSP capital allocation in the period from 2025 to 2027.

The interaction is asymmetric across PSP categories and member states. In jurisdictions where SCT Inst adoption was already high before the IPR's adoption, including the Netherlands and the Baltic states (Estonia, Latvia, and Lithuania), PSPs have already absorbed a significant share of the technical investment required for IPR compliance, and the marginal cost of the remaining obligation is lower. In those same jurisdictions, digital euro pilots are more likely to be advanced, but the PSPs' stronger financial position means the concurrent obligation is more manageable. In jurisdictions where SCT Inst adoption was low, specifically parts of southern Europe and several central and eastern European member states outside the Baltic group, the IPR compliance cost is higher, the digital euro distribution infrastructure is less developed, and PSP balance sheets are more constrained. The compounding pressure is therefore greatest precisely where infrastructure capacity is weakest, a distributional pattern that the uniform deadline architecture does not accommodate.

Pricing parity and revenue model adaptation. The pricing-parity rule produces a revenue compression effect that is more significant for smaller institutions than for large universal banks. For a small savings bank or cooperative credit institution whose payment services revenue includes a material component from transfer fees differentiated by speed or channel, the mandatory elimination of that differential removes a cross-subsidy mechanism. The institution must either accept reduced payment-services revenue or recover costs through account maintenance fee increases or product-bundle restructuring. This adaptation is feasible but requires pricing model redesign that takes time and creates customer communication risk. For institutions facing this pressure simultaneously with IPR technical investment and digital euro distribution preparation, the aggregate management bandwidth demand is non-trivial.

Nominal coverage versus genuine coverage. The most significant structural insight from this analysis is that the IPR's deadlines will likely produce nominal universal coverage, defined as a state in which every in-scope PSP has a regulatory-compliant instant-payment offering, without necessarily producing genuine universal coverage in the sense of a payment system where instant settlement is the default, equally accessible, and equally resilient option for all euro-area users. Nominal coverage is satisfied by a PSP that has contracted with a third-party processor, set its instant-payment fee at exactly the level of its standard-transfer fee, and passed its verification-of-payee obligation to the processor. Genuine coverage requires that the underlying infrastructure is available with sufficient reliability, capacity, and independence to function as a systemic utility. A PSP that achieves formal compliance without substantive operational readiness at the processor layer it depends on contributes to the nominal coverage count while leaving the system's resilience dependent on the processor's continuity. The gap between these two states is the governance question that post-2027 regulatory attention will need to address.

Conclusion: Scheduled Transformation of the Euro-Area Payments Infrastructure

The Instant Payments Regulation and PSD3 constitute a legislative commitment to universal euro-area instant-payment coverage within a fixed calendar sequence. This paper has examined the mechanism by which that commitment is translated into operational obligation, identified the structural conditions under which the mechanism succeeds or produces incomplete outcomes, and traced the interaction with the digital euro legislative package as a compounding variable.

The central claim of this paper is that the IPR's phased deadline architecture functions as a coordination device that resolves the network-externality deferral failure that characterised the voluntary SCT Inst regime. The mechanism is technically well-designed: the receiving-before-sending sequencing generates informational spillovers that lower the second-stage investment threshold, the pricing-parity rule established in Article 5 eliminates the revenue-based incentive to suppress uptake, and the verification-of-payee and real-time fraud-screening requirements create a quality floor that prevents formal compliance without substantive operational readiness. These features collectively constitute a more sophisticated regulatory instrument than a simple binary mandate.

The mechanism's principal vulnerability lies in the compliance pathway it implicitly rewards. By imposing uniform obligations on a heterogeneous PSP population without specifying how compliance must be achieved, the IPR creates the conditions for a concentrated third-party processing tier to emerge as the dominant compliance vehicle for smaller institutions. This concentration achieves the metric of universal coverage while relocating the system's operational risk from a distributed set of PSP nodes to a small set of processor hubs. The European Banking Authority and national competent authorities possess supervisory tools under PSD3's outsourcing and operational resilience provisions that could address this concentration, but those tools have not been explicitly calibrated to the IPR compliance scenario.

For payment system resilience, the implications extend across several vectors. Post-2027 supervisory attention should be directed at the processor tier rather than at individual PSP compliance status. The relevant resilience metrics are the share of instant-payment transaction volume passing through processors subject to concentration risk; the settlement-money type, central bank versus commercial bank, through which those processors operate; the contractual continuity obligations and substitutability provisions governing the relationship between dependent PSPs and their processors; and the operational continuity standards applicable to processors whose aggregate volume reaches systemic significance. These metrics require a monitoring framework that neither the IPR nor PSD3 currently mandates in explicit terms.

For competitive dynamics, the pricing-parity rule changes the terrain on which PSPs compete for payment account business in ways that extend beyond fee revenue. When instant settlement is a commodity feature with a mandated price ceiling, differentiation must occur through user experience design, account feature depth, data-driven service personalisation, and the quality of ancillary financial products bundled with payment accounts. This structural shift generates selective pressure that favours institutions with strong product development capability and customer analytics capacity over those whose competitive position rested on processing margins. The medium-term consequence is consolidation among smaller PSPs whose cost base cannot be sustained through non-payment revenue streams alone. The pace of that consolidation will depend on member-state supervisory tolerance for PSP exit and the availability of third-party processing as a cost-reduction mechanism that delays, rather than prevents, that exit.

For future regulatory design, the IPR and PSD3 dyad offers a template that differs from the SEPA DD model in a structurally important respect: by distributing compliance obligations across a phased sequence of category-specific deadlines rather than a single industry-wide end-date, the IPR reduces the political feasibility of a blanket deadline extension of the kind that preceded Regulation (EU) No 248/2014. Future applications of this template, whether in the context of digital euro distribution, cross-border instant settlement with non-euro member states, or next-generation payment infrastructure, should incorporate explicit provisions addressing the concentration risk that emerges when the compliance pathway runs through a small number of third-party processors. Such provisions could take the form of secondary regulation specifying processor-tier concentration thresholds, supervisory guidance on PSP due diligence for processor selection, or mandatory redundancy requirements for PSPs whose processor dependency exceeds a defined volume threshold. The absence of such provisions in the current IPR text represents a design gap that can be closed through secondary regulation or supervisory guidance without reopening the primary legislative text.

The January 2027 deadline for payment institutions and EMIs will mark the nominal completion of the euro-area coverage mandate. The supervisory and governance work required to convert that nominal coverage into a structurally resilient, competitively dynamic, and equitably accessible instant-payment infrastructure extends across the period following that date and calls for a monitoring and enforcement framework calibrated to the processor-tier risks that the phased compliance mechanism has created.

Evidentiary Gaps and Boundaries of Analysis

-

Absence of participant-level compliance data. The primary evidentiary gap in this analysis is the absence of current, institution-level data on IPR compliance status across euro-area PSPs. The European Banking Authority had not published a comprehensive IPR compliance monitoring report at the time of writing. The coverage projections in Section 5 are therefore derived from structural inference (deadline architecture, participant taxonomy, and known SCT Inst adoption patterns) rather than from observed compliance rates. The conclusion that lagging member states face greater compliance pressure is directionally well-supported by the pre-IPR SCT Inst adoption literature, but the magnitude of that gap is not quantified in this paper.

-

Unmodelled spillover effects from digital euro development. The interaction between IPR compliance obligations and digital euro distribution requirements is identified at the level of mechanism and temporal overlap, but the paper does not model the magnitude of the capital-allocation conflict. The scale of that conflict depends on the specific technical architecture of the digital euro distribution system, the fee structure imposed on PSPs for distribution services, and the pace at which digital euro pilots progress to general deployment. All three of these parameters were subject to legislative and supervisory uncertainty at the time of writing, preventing quantitative modelling.

-

Third-party processor concentration proxy is structural, not measured. The finding that third-party processor concentration represents the principal systemic risk in post-2027 coverage scenarios is derived from structural inference using the conditions identified by Dezem et al. [10], the known architecture of TIPS and RT1, and historical consolidation patterns in related markets. No dataset of actual processor market share in IPR-compliant instant-payment delivery was available. The concentration risk identification is therefore a mechanism hypothesis rather than an empirically verified finding.

-

Regulatory change risk post-2027. The analysis treats the IPR and PSD3 texts as stable instruments. Both are subject to legislative amendment, and the PSD3 proposal in particular remained in trilogue at the time of writing. Material amendments to the participant category definitions, exemption conditions, or enforcement provisions in PSD3 could alter the coverage mechanism in ways this paper does not anticipate.

-

Non-euro member state dynamics are underanalysed. The paper concentrates its analysis on euro-area PSPs. The IPR also applies to PSPs in non-euro EU member states, subject to different timelines and conditions. The interaction between the euro-area coverage mechanism and non-euro member state obligations, particularly for cross-border instant transfers denominated in euros but processed through non-euro member state PSPs, is not fully examined here.

Next Analytical Directions

Real-time compliance coverage surveys. The most direct extension of this work is a member-state-level survey of IPR compliance status, conducted at intervals corresponding to each phase deadline. Such a survey would require access to national competent authority supervisory data or structured self-reporting by PSPs. The European Banking Authority's forthcoming IPR compliance monitoring reports will provide the primary instrument for this work once published. The specific metric to be constructed is the share of payment accounts held at fully IPR-compliant PSPs as a fraction of total euro-area payment accounts, disaggregated by member state and PSP category.

Cost-benefit modelling at the participant level. The pricing-parity rule and the infrastructure investment requirement create institution-specific financial impacts that vary with PSP size, existing IT architecture, and transaction volume mix. A cost-benefit model calibrated to representative PSP archetypes (large universal bank, medium regional bank, small payment institution, EMI) would quantify the revenue compression and investment cost for each archetype and identify the conditions under which third-party outsourcing is financially dominant over in-house build. This modelling would use the decision framework from Dezem et al. [10] as its methodological foundation.

Concentration risk measurement. A focused study of the third-party processor market for IPR-compliant instant-payment services would measure the share of compliant transaction volume processed by the top five non-bank processors in each member state. The data instrument for this work is transaction-level reporting under the IPR's monitoring provisions, supplemented by processor-level operational data where available. The analysis should distinguish between volume concentration on TIPS-settling processors and volume concentration on RT1-settling processors, given the distinct risk profiles of central-bank-money and commercial-bank-money settlement documented in Section 4.

Digital euro and IPR interaction scenarios. Scenario planning for the 2025-2027 compliance window should model three trajectories: accelerated digital euro rollout coinciding with peak IPR compliance investment; delayed digital euro deployment that removes the concurrent-obligation pressure; and a partial rollout confined to pilot jurisdictions. Each scenario carries distinct implications for PSP capital allocation, third-party processor demand, and the competitive topology of the euro-area payments market.

Figures and Tables

Figure 1

Figure 2

Figure 3

Figure 4

Table 1

| cluster_idx | cluster_short | n_cards | total_words | mean_words | mean_sent_len | sum_kw_Instant_Payments | sum_kw_Digital_Euro | sum_kw_Open_Banking | sum_kw_Global_Benchmarks | sum_kw_Decentralisation | sum_kw_Regulation |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | Instant Payments & RT Infra | 3 | 485 | 161.66666666666666 | 20.666666666666668 | 1 | 0 | 1 | 1 | 0 | 0 |

| 1 | Digital Euro | 4 | 787 | 196.75 | 28.107142857142858 | 0 | 4 | 0 | 2 | 0 | 0 |

| 2 | EU Data / Open Banking | 4 | 725 | 181.25 | 25.892857142857142 | 0 | 0 | 2 | 2 | 1 | 0 |

| 3 | Global Fintech / DPI | 4 | 762 | 190.5 | 27.214285714285715 | 0 | 0 | 0 | 9 | 0 | 0 |

| 4 | Decentralisation / CBDC | 2 | 442 | 221.0 | 31.57142857142857 | 0 | 2 | 0 | 0 | 5 | 0 |

Table 2

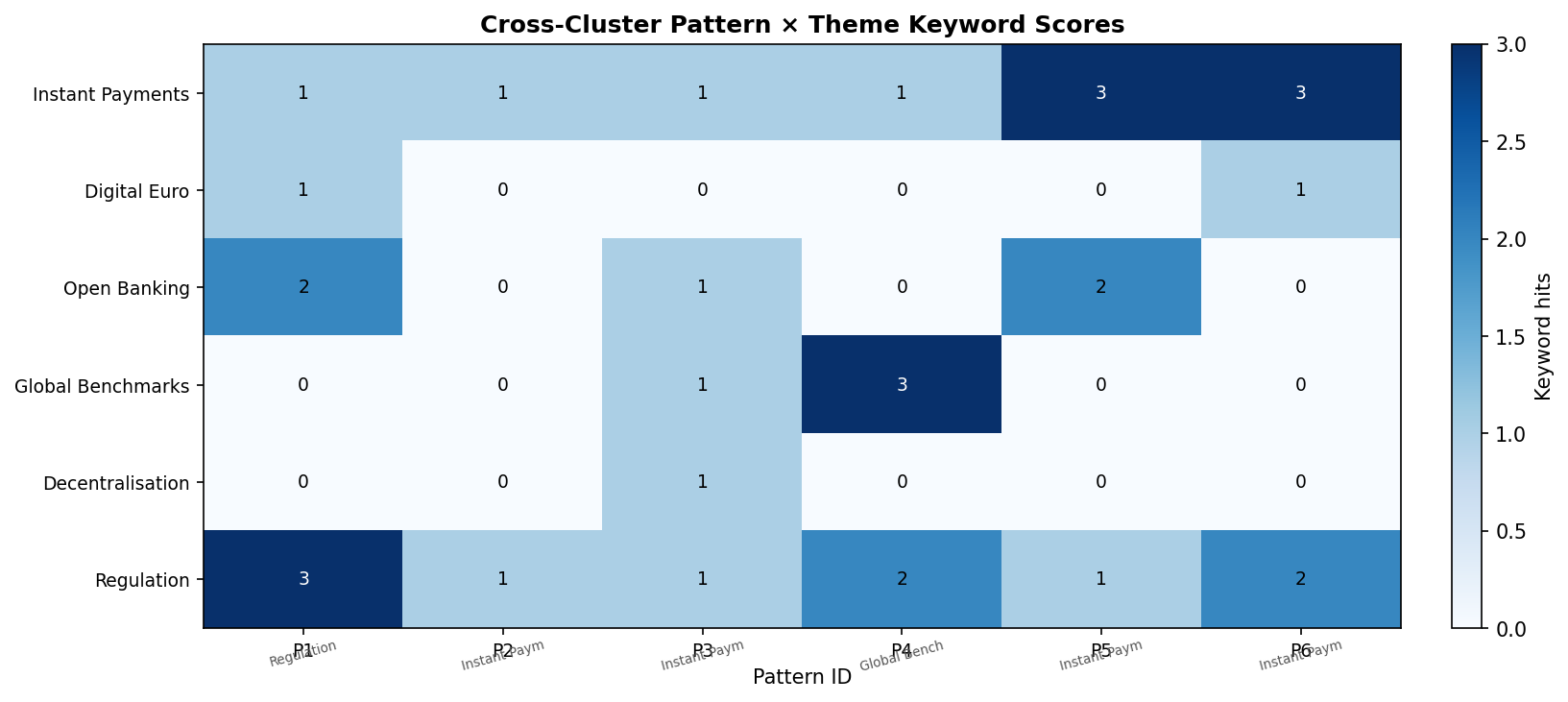

| pattern_id | word_count | sentence_count | dominant_theme | score_Instant_Payments | score_Digital_Euro | score_Open_Banking | score_Global_Benchmarks | score_Decentralisation | score_Regulation |

|---|---|---|---|---|---|---|---|---|---|

| 1 | 55 | 2 | Regulation | 1 | 1 | 2 | 0 | 0 | 3 |

| 2 | 44 | 3 | Instant Payments | 1 | 0 | 0 | 0 | 0 | 1 |

| 3 | 54 | 3 | Instant Payments | 1 | 0 | 1 | 1 | 1 | 1 |

| 4 | 55 | 2 | Global Benchmarks | 1 | 0 | 0 | 3 | 0 | 2 |

| 5 | 50 | 2 | Instant Payments | 3 | 0 | 2 | 0 | 0 | 1 |

| 6 | 52 | 2 | Instant Payments | 3 | 1 | 0 | 0 | 0 | 2 |

References

-

Demertzis, M., Merler, S., & Wolff, G. B. (2017). Capital Markets Union and the Fintech Opportunity. Oxford University Press.

-

Mancini Griffoli, T., Martínez Pería, M. S., Agur, I., Ari, A., Kiff, J., & Popescu, A. (2018). Casting Light on Central Bank Digital Currencies. International Monetary Fund.

-

Hanedar, E., Alonso, C., Uña, G., Prihardini, D., Bhojwani, T., & Zhabska, K. (2023). Stacking up the Benefits: Lessons from India's Digital Journey. International Monetary Fund.

-

Lannquist, A. (2023). Central Bank Digital Currency's Role in Promoting Financial Inclusion. International Monetary Fund.

-

Melo, F. C. S. A., Sugimoto, N., Bains, P., & Ismail, A. (2022). Regulating the Crypto Ecosystem. International Monetary Fund.

-

Rousset, M., Lambert, F., Martínez Torres, J. A., Herrera, L., Ramos, G., & Gershenson, D. (2021). Fintech and Financial Inclusion in Latin America and the Caribbean. International Monetary Fund.

-

Coche, E., Kolk, A., & Dekker, M. (2024). Navigating the EU data governance labyrinth: A business perspective on data sharing in the financial sector. Alexander von Humboldt Institute for Internet and Society.

-

Pastor Sempere, M. C. (2025). Governance and Control of Data and Digital Economy in the European Single Market. Springer International Publishing.

-

Zatti, F., & Barresi, R. G. (2025). The Digital Euro Package: From Legal Tender to Payment Services Providers. Springer International Publishing.

-

Dezem, V., Sachan, S., Macedo, M. Á. S., & Longaray, A. A. (2024). Optimal data-driven strategy for in-house and outsourced technological innovations by open banking APIs. Springer Science+Business Media.

-

Pastor Sempere, C. (2025). The Legal Framework for New Digital Assets, Identities, and Data Spaces. Introduction. Springer International Publishing.

-

Mula, K. (2025). Real-Time Revolution: The Evolution of Financial Transaction Processing Systems. European Journal of Computer Science and Information Technology.

-

Negrea, C. I., Scarlat, E. M., Horătău, I., & Manta, O. (2025). Governing Financial Innovation Through Institutional Learning: Lessons from Romania's Fintech Innovation Hub. Preprints.org.

-

Gortsos, C. V. (2026). The European Commission's Proposal for an EU Regulation "On the Establishment of the Digital Euro": Its Provisions on the Legal Tender Status of the Digital Euro and on the Limits Imposed to Its Use as a Store of Value and as a Means of Payment. De Gruyter.