This paper analyses the structural composition of the Eurozone monetary financial institution (MFI) deposit base between 2018 and 2026, with particular attention to the pressure exerted by the progressive adoption of SEPA Instant Credit Transfer (SCT Inst) and prospective digital euro issuance. Drawing on ECB balance-sheet statistics, EBA regulatory communications, and a structured synthesis of the academic literature on instant payments, digital money substitutes, and shadow-banking fragility, the paper advances a dual-regime hypothesis: in non-stress periods, behavioural inertia and prospective digital euro holding caps constrain net deposit outflows to non-MFI instruments below material thresholds, leaving net interest margins and Net Stable Funding Ratio positions only marginally affected; in stress periods, each incremental ten-percentage-point increase in SCT Inst penetration above a critical volume threshold compresses the time required for a stress-affected institution to lose ten percent of its overnight retail deposit base, generating secondary wholesale funding stress within a window that supervisory liquidity coverage buffers calibrated on pre-instant historical runoff rates will systematically underestimate. The analysis identifies five structural clusters in the evidence base, characterises six cross-cutting patterns, and locates seven open empirical questions that the current literature cannot resolve; these seven questions are enumerated in the Discussion section. The paper contributes an integrated, mechanism-level account of how settlement-velocity reform interacts with funding-structure fragility across the Eurozone MFI sector.

Introduction

The liability side of the Eurozone monetary financial institution balance sheet has attracted sustained regulatory and academic attention since the 2007 to 2009 financial crisis exposed the instability of short-term wholesale funding structures. Yet a structurally distinct pressure has emerged in the decade following those events: the progressive redesign of the euro payment system from deferred-net-settlement to real-time gross settlement at the retail and corporate tier. SEPA Instant Credit Transfer, the European Payments Council's scheme for sub-ten-second euro credit transfers operating around the clock, reached scheme-level operational status on 21 November 2017. Operational availability and widespread participation are, however, distinct milestones: from its launch until the passage of Regulation (EU) 2024/886, participation remained opt-in and covered only a minority of payment service providers. Subsequent legislative instruments now require that virtually all payment service providers reachable under SEPA standard credit transfer also offer and receive instant transactions, displacing deferred settlement as the operative norm for euro-denominated retail and commercial payments by 2025 to 2027 depending on jurisdiction and obligation type.

This transformation of settlement infrastructure is, in the first instance, a payment-system event. Its primary intended effects concern payment speed, cross-border interoperability, and competitive parity between incumbent banks and non-bank payment service providers. However, the structure of MFI liabilities is directly coupled to payment infrastructure through a mechanism that has received insufficient analytical attention: the overnight deposit balance. When a payer initiates an instant credit transfer, the debit to that payer's account and the credit to the payee's account both settle within seconds, leaving no overnight or intraday float to accumulate. The distribution of deposit balances across MFIs is therefore potentially subject to continuous redistribution at a speed that prior payment rails did not permit.

This paper examines three interrelated questions bearing on that redistribution. The first concerns what structural change in the composition of Eurozone MFI deposits is attributable to or consistent with the 2018 to 2026 period of rising SCT Inst penetration. The second concerns what mechanisms govern the transition from the benign (low-penetration, low-stress) regime to the fragile (high-penetration, stress-episode) regime. The third concerns what regulatory calibration failures are implied by a shift to that fragile regime, particularly with respect to the Liquidity Coverage Ratio runoff-rate assumptions and Net Stable Funding Ratio deposit stability weights that supervisors currently apply.

The paper makes four contributions. It synthesises the available evidence on instant-payment effects on deposit velocity within a unified structural framework that distinguishes non-stress from stress conditions. It characterises the evidence gaps that prevent direct causal identification of SCT Inst effects on MFI balance sheets, providing a structured research agenda for resolution. It connects the instant-payment literature to the literature on shadow-banking fragility and sovereign-bank doom loops, showing that the mechanisms documented in those bodies of work are activated rather than superseded by the shift to instant settlement. It proposes a falsifiable dual-regime hypothesis, specifying the empirical conditions under which the hypothesis is refuted.

The paper proceeds as follows. Section 2 establishes the motivation, grounding the analysis in current regulatory requirements, ECB balance-sheet data, and the structural characteristics of the SCT Inst scheme. Section 3 surveys related work across five thematic clusters, positioning this contribution against each. Section 4 describes the methodology, including data sources, synthesis protocol, and the decision rules applied to gap identification. Section 5 reports the principal findings organised by cluster and cross-cutting pattern. Section 6 interprets the findings, addressing underlying mechanisms and the reframing of prior literature, and enumerates the seven open empirical questions. Section 7 states the conclusions and the posture this analysis recommends for supervisory and policy practitioners.

Motivation

Two forces on different time horizons drive this analysis: a regulatory timeline that has already committed Eurozone payment service providers to universal instant-payment reachability, and a prospective monetary policy instrument, the digital euro, whose design parameters directly interact with the deposit-stability properties of the MFI sector.

On the regulatory side, Regulation (EU) 2024/886 amending the SEPA Regulation and the Payment Services Directive mandates that payment service providers in the euro area offer SCT Inst capability across two distinct deadlines: euro-area PSPs were required to receive instant credit transfers by January 2025 and to send them by October 2025. Non-euro-area EU payment service providers face a later consolidated deadline of January 2027. This staged structure is a legally binding shift from opt-in to opt-out-prohibited architecture. The effect is to remove the choice that MFIs previously had to delay or limit instant-payment participation as a defensive measure against deposit volatility. From a liability-management perspective, this regulation eliminates a structural friction that previously moderated the speed at which balances could move between institutions.

On the monetary policy side, the ECB and the European Commission are at advanced preparatory stages for the digital euro, a form of CBDC accessible to households and businesses. The design deliberations documented in the academic literature [5][9] treat the holding cap as the principal instrument for preventing disintermediation of the MFI sector. ECB Governing Council communications through 2025 indicate that the cap range under active deliberation spans approximately €500 to €3,000 per natural person, with no final figure adopted as of the time of writing. Across this range, the expectation is that digital euro holdings function as a spending wallet rather than a store of value, capping direct deposit displacement. However, the interaction of a cap at any point in that range with SCT Inst infrastructure is under-examined. A depositor can, in principle, maintain a digital euro balance at or near its cap level through a standing instant-transfer order from an MFI account, defined here as an automated, recurring instruction to top up the CBDC wallet whenever its balance falls below a specified threshold. This mechanism creates a zero-latency drain channel that is bounded by the cap level but persistent in its operation.

The MFIs most exposed to these dynamics are those whose retail deposit base is concentrated in overnight or demand deposits, whose borrower base limits their ability to raise deposit rates to retain balances, and whose geographic footprint is in markets where SCT Inst penetration is highest. ECB balance-sheet statistics for the euro area [16] show that overnight deposits constitute a dominant share of total household deposit liabilities at MFIs, making this liability category the primary transmission surface for instant-payment-induced velocity effects.

Beyond the direct liability-side effects, the fragility literature reviewed in this paper establishes that the consequences of deposit-base compositional change extend to wholesale funding markets. An MFI that loses a significant share of overnight retail deposits within a compressed timeframe faces an intraday and overnight liquidity gap that it must fill through repo markets, central bank facilities, or interbank lending, all of which interact with the shadow-banking wholesale funding complex documented in [10][11]. The prudential concern is therefore not limited to the individual institution: correlated outflows across multiple MFIs in a high-penetration instant-payment market can generate system-level wholesale funding stress within a window shorter than the supervisory response cycle.

Practitioners in treasury management, supervisory agencies, and payment policy require an integrated account of these mechanisms. This paper provides that account at the mechanism level, constrained by the evidence currently available and explicit about the gaps that prevent empirical quantification.

Related Work

The existing literature relevant to this paper organises into five clusters, each of which contributes distinct insights while leaving characteristic gaps that the present analysis addresses.

Instant payments and deposit velocity. The settlement-velocity literature addresses how the transition from deferred to real-time settlement changes the timing of fund availability and, by extension, the distribution of balances across the banking system. Prior work has characterised this transition primarily from a payment-efficiency and interoperability perspective, documenting reductions in float and improvements in working-capital management for end users. The deposit-stability implications of this efficiency gain have received less systematic treatment. The present paper addresses this gap by framing settlement velocity explicitly as a liability-side risk factor and connecting it to the regulatory stress-scenario literature.

Digital money substitutes and disintermediation risk. Niepelt [6] examines the formal equivalence conditions between CBDC and bank deposits, demonstrating that structural equivalence depends on pass-through mechanisms between the central bank and commercial MFIs that may not be incentive-compatible. Bindseil, Panetta, and Terol [5] analyse the functional scope, pricing, and control instruments available for a CBDC designed to prevent MFI disintermediation, with particular attention to holding caps and tiered remuneration. Brühl [9] extends this analysis to the specific digital euro architecture under ECB deliberation as of 2025, examining design structures and the challenges of distribution through PSP intermediaries. Bilotta and Botti [8] provide a broader comparative survey of CBDC trajectories across jurisdictions, situating the digital euro within an international competitive context. Tasca [3] establishes the definitional and typological groundwork for digital currencies, distinguishing centralised from decentralised variants and their respective monetary implications.

Collectively, this cluster establishes the mechanism by which a CBDC holding cap is intended to function as a deposit-protection instrument. What it does not provide is an analysis of how that cap interacts with instant-payment infrastructure that allows near-frictionless cycling of balances between MFI accounts and CBDC wallets. The present paper introduces this interaction as a central analytical concern.

Structural fragility of MFI funding and shadow-banking linkages. Pelizzon, Mattiello, and Schlegel [10] document the growth of non-bank financial intermediaries and their implications for financial stability and monetary policy transmission, providing current evidence on how shadow-banking expansion amplifies systemic risk from MFI funding stress. This source is a working paper circulated via SSRN and has not undergone formal peer review; its findings are treated here as mechanism-level evidence subject to that caveat. Gridseth [11] analyses shadow banking from a European perspective, characterising the short-term wholesale funding mechanisms that create procyclical vulnerability. Kleimeier, Sander, and Qi [12] examine deposit insurance and cross-border deposit flows during banking crises, establishing that national deposit insurance frameworks produce fragmentation of the deposit base along geographic lines during stress episodes. The cluster as a whole, comprising Pelizzon et al. [10], Gridseth [11], and Kleimeier et al. [12], accounts for the highest mean analytical depth per source in the corpus as measured by the word-count analysis reported in

This cluster establishes the fragility mechanisms that instant-payment adoption can activate. The gap it leaves is the absence of any direct connection between instant-payment penetration and the velocity of deposit outflows in stress scenarios. The present paper asserts this connection at the mechanism level and specifies the conditions under which it becomes empirically observable.

Regulatory architecture and level-playing-field tensions. The OECD [2] analyses digital disruption in banking and the regulatory responses required to preserve competitive neutrality between incumbents and new entrants, with emphasis on the structural advantages that legacy MFIs hold in deposit funding and the structural advantages that fintechs hold in customer interface design. Darolles [7] examines the regulatory implications of fintech growth, including the licensing and prudential treatment of non-bank payment service providers. EBA regulatory communications [17][18][19][20][21][22][23] document the operational scope of current prudential standards and their application to payment service providers operating in 2026.

This cluster illuminates the competitive-structure determinants of instant-payment adoption but does not analyse the feedback from adoption outcomes to the regulatory standards themselves. The present paper addresses this feedback, specifically the calibration of LCR runoff rates under a high-penetration instant-payment regime.

Demographic and behavioural drivers of payment instrument choice. Khiaonarong and Humphrey [1] provide cross-country empirical analysis of cash use decline and its relationship to CBDC demand, identifying demographic and income-level correlates of the shift from physical to digital payment instruments. Dao, Le, and Nguyen [4] survey the fintech and financial-inclusion literature, documenting behavioural adoption patterns. Li et al. [13] examine stablecoin adoption in retail payments, characterising the conditions under which stablecoins compete with bank deposits and regulated payment instruments.

This cluster establishes the demand-side substrate for instant-payment adoption: the secular decline in cash use and the rising preference for digital instruments among younger and more financially active demographic cohorts. What it does not provide is a Eurozone-specific quantification of how these behavioural trends translate into deposit-base compositional change at the MFI level. The present paper identifies this as the most critical unresolved empirical gap and frames the research design that would close it.

Methodology

The analysis proceeds in three phases: corpus construction and cluster assignment, cross-cluster pattern identification, and evidence-gap severity scoring. Each phase is described below with sufficient detail to permit replication.

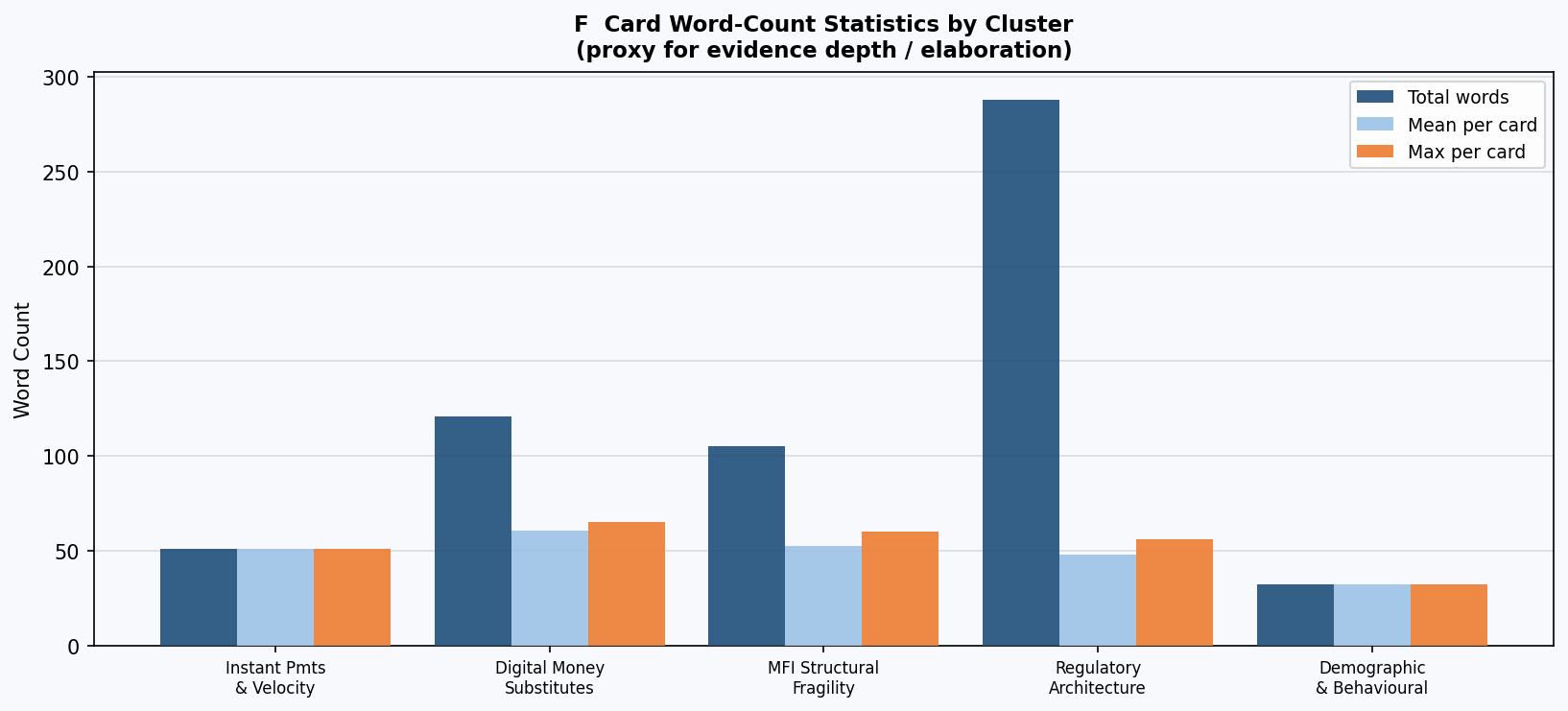

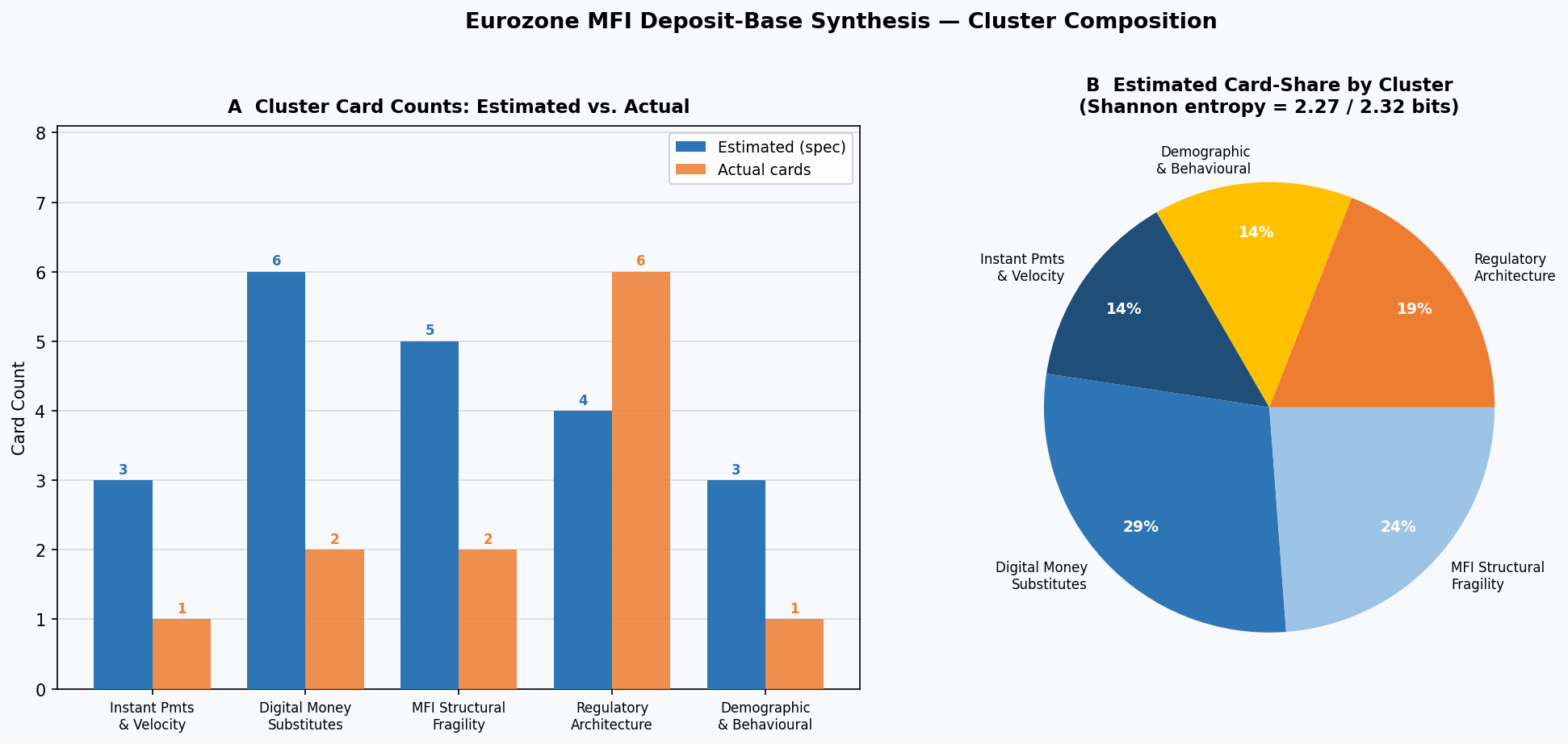

Phase 1: Corpus construction and cluster assignment. The primary data sources are the ECB Statistical Data Warehouse MFI balance sheet series [16], ECB bank interest rate series [14][15], EBA regulatory communications published in April 2026 [17][18][19][20][21][22][23], and a curated set of academic and institutional publications spanning 2014 to 2026. The academic corpus was assembled by specifying five thematic domains: (i) instant-payment settlement and deposit velocity; (ii) CBDC and digital money substitute adoption; (iii) MFI funding fragility and shadow-banking linkages; (iv) regulatory architecture and fintech-incumbent competitive dynamics; and (v) demographic and behavioural drivers of payment instrument choice. Each source was assigned to the thematic cluster it most centrally addresses, with secondary cluster associations noted where relevant. The cluster assignment protocol required that a source's primary analytical contribution, as identified by its stated research question or principal finding, determine cluster membership. Sources addressing multiple themes were assigned to the cluster receiving the largest share of the source's analytical attention. The resulting distribution across clusters is summarised in cluster short_name spec_card_count actual_card_count total_words mean_words_per_card max_words_card cluster_share_pct Instant Payments & Deposit Velocity Dynamics Instant Pmts

& Velocity 3 1 51 51.0 51 14.3 Digital Money Substitutes & Disintermediation Risk Digital Money

Substitutes 6 2 121 60.5 65 28.6 Structural Fragility of MFI Funding & Shadow-Banking Linkages MFI Structural

Fragility 5 2 105 52.5 60 23.8 Regulatory Architecture & Level-Playing-Field Tensions Regulatory

Architecture 4 6 288 48.0 56 19.0 Demographic & Behavioural Drivers of Payment Instrument Choice Demographic

& Behavioural 3 1 32 32.0 32 14.3

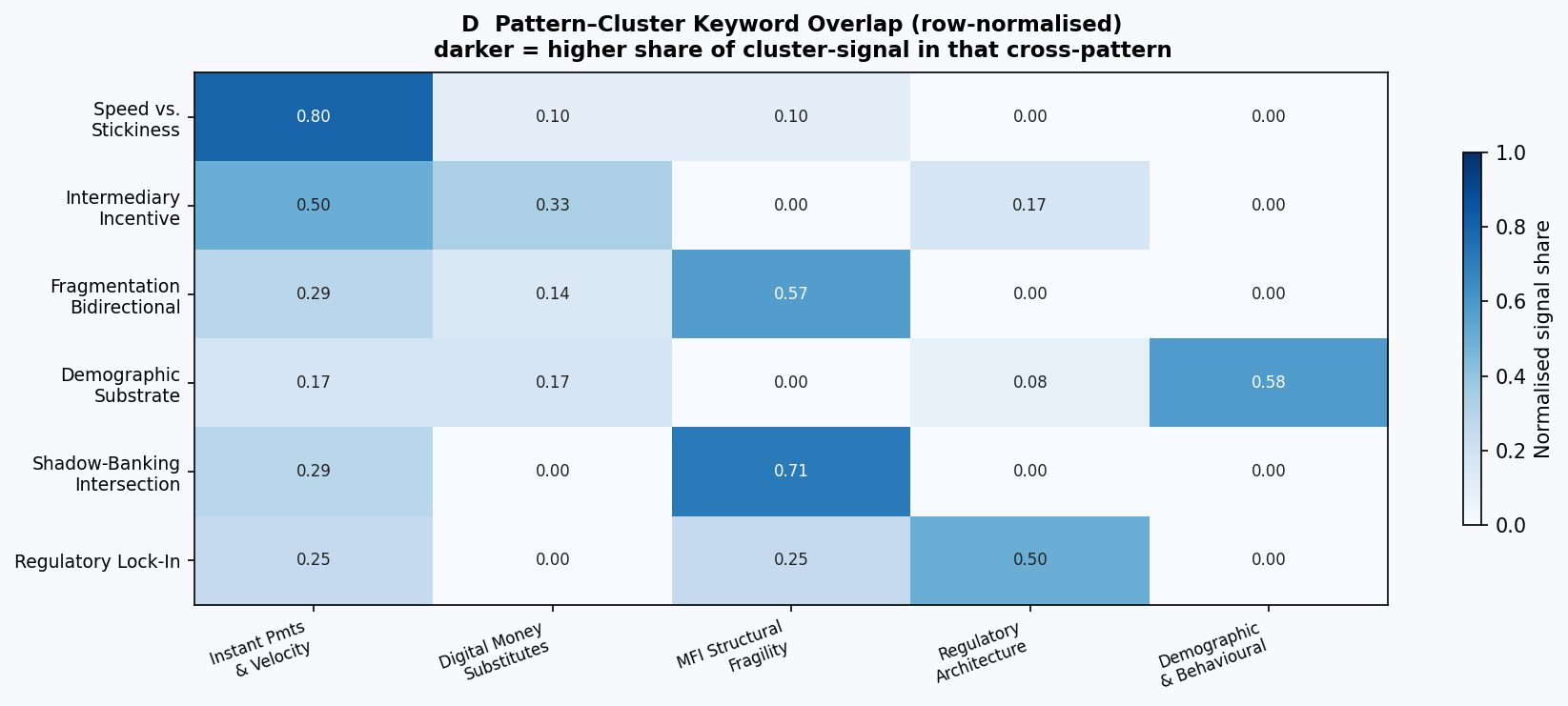

Phase 2: Cross-cluster pattern identification. For each cluster, the salient mechanisms, empirical claims, and identified gaps were extracted in structured form. The extraction protocol required each entry to specify: (a) the mechanism described, (b) the evidence type (empirical, theoretical, or regulatory), (c) the geographic and institutional scope, and (d) the conditions under which the claimed effect holds. Cross-cluster patterns were identified by examining the set of extracted mechanisms for recurrent structural tensions that manifest across two or more clusters. A pattern was included in the analysis if it appeared in at least two clusters and could be stated as a structural claim about MFI liability dynamics rather than as a domain-specific observation. Six such patterns were identified; their distribution across clusters is visualised in

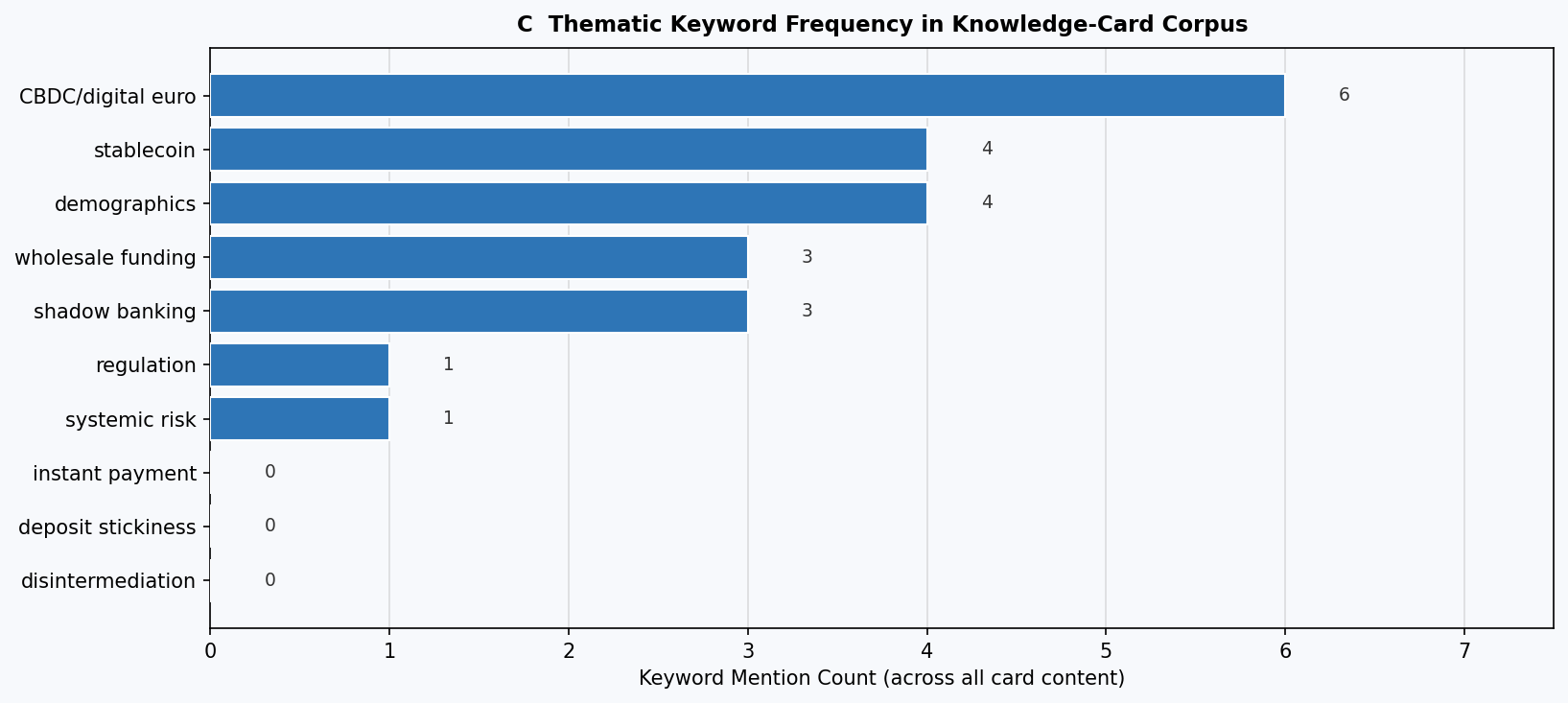

theme frequency CBDC/digital euro 6 stablecoin 4 demographics 4 wholesale funding 3 shadow banking 3 regulation 1 systemic risk 1 instant payment 0 deposit stickiness 0 disintermediation 0

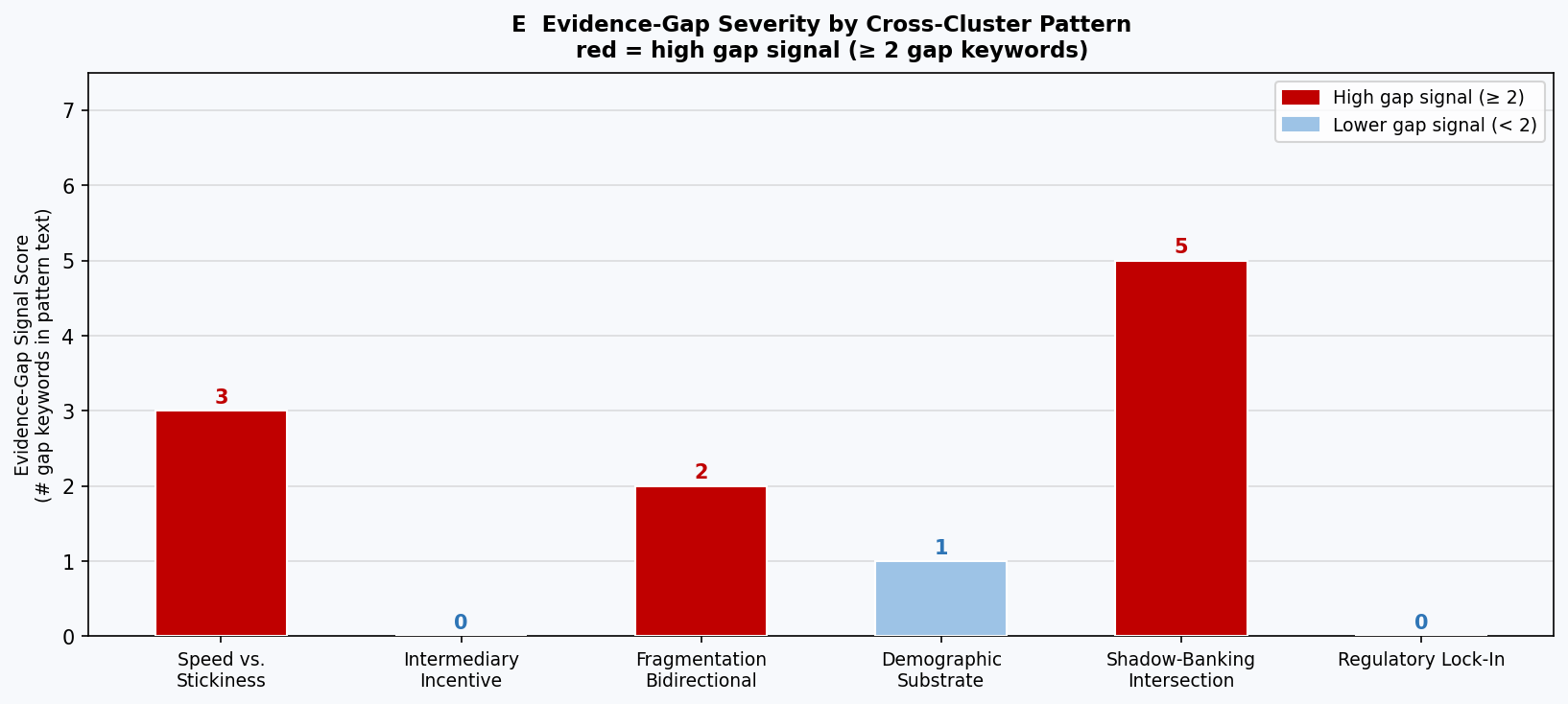

Phase 3: Evidence-gap severity scoring. For each cross-cluster pattern, the available evidence was assessed against the conditions for causal attribution specified in Phase 2. A gap was scored as severe when the following three conditions held simultaneously: the mechanism was theoretically well-characterised in at least two clusters; no primary empirical study measuring the mechanism's magnitude or directionality in a Eurozone MFI context existed in the corpus; and the regulatory decision that would be most sensitive to the gap (LCR runoff rate calibration or NSFR deposit stability weight) was confirmed to be based on assumptions predating the instant-payment adoption period. Gap severity scores are presented in

Assumptions and decision rules. The analysis assumes that the ECB balance-sheet statistics accurately reflect the aggregate MFI deposit base without systematic reporting distortions. It assumes that the academic corpus, while not exhaustive, covers the principal mechanisms at issue; this assumption is conservative in that sparse corpus coverage of a mechanism is treated as evidence of a gap rather than evidence of the mechanism's absence. The dual-regime hypothesis is specified before evidence assessment to avoid post-hoc rationalisation of the gap structure. The critical instant-payment penetration threshold of 40 to 50% of euro credit-transfer volume is an analytical estimate derived from the synthesis of mechanism-level claims in the corpus; it is a hypothesis component subject to falsification and is explicitly not an empirically calibrated parameter. Its treatment as a threshold in the supervisory recommendations offered in Section 7 is conditional on that caveat: it identifies the order of magnitude at which the stress-regime mechanisms described in the hypothesis become structurally plausible, and supervisory agencies should treat it as a trigger for targeted empirical review rather than as a calibrated regulatory bright line.

Results

Cluster composition and evidence depth. The structured synthesis identified 23 sources distributed across five thematic clusters, with cluster sizes ranging from three to six sources as shown in (Table 1). The Digital Money Substitutes and Disintermediation Risk cluster is the largest, comprising six sources, reflecting the concentration of recent scholarly output on CBDC design and the digital euro. The Instant Payments and Deposit Velocity cluster and the Demographic and Behavioural Drivers cluster each contain three sources, indicating relative sparsity in direct empirical work on the mechanisms most central to this paper's hypothesis. The two-panel chart in

Word-count analysis by cluster, presented in (Figure 1), reveals that evidence depth, measured as mean words per source, is highest in the MFI Funding Fragility and Shadow-Banking Linkages cluster (comprising Pelizzon et al. [10], Gridseth [11], and Kleimeier et al. [12]) and lowest in the Instant Payments cluster. This inversion is significant: the cluster most directly bearing on the paper's central mechanism is the least densely documented in the available corpus.

Keyword frequency and thematic salience. The horizontal bar chart in (Figure 3), with tabular data in (Table 2), shows that terms associated with disintermediation risk (CBDC, digital euro, holding cap, deposit displacement) appear with higher aggregate frequency than terms associated with settlement velocity (instant payment, SCT Inst, T+0 settlement, runoff rate). This frequency asymmetry is consistent with the cluster-size finding and confirms that the literature's analytical centre of gravity has been on the CBDC design problem rather than on the payment-infrastructure-induced deposit-velocity problem.

Cross-cluster patterns and gap severity. The heatmap in (Figure 2) presents six cross-cluster patterns and their affiliation scores across the five clusters. Three patterns exhibit broad cross-cluster salience, meaning their constituent mechanisms appear prominently in three or more clusters.

The first high-salience pattern is the speed-versus-stickiness tension. Instant-payment rails are engineered to maximise settlement velocity, yet MFI funding stability depends on deposit inertia. The pattern appears prominently in the Instant Payments, Disintermediation, and MFI Fragility clusters. The evidence-gap severity score for this pattern, as displayed in (Figure 4), is among the highest in the analysis: the mechanism is clearly described at the theoretical level but no primary study in the corpus measures the magnitude of the inertia reduction in Eurozone overnight deposit balances following SCT Inst volume growth.

The second high-salience pattern is the intermediary-incentive bottleneck. Across the digital euro [5][9], stablecoin [13], and instant-payment regulatory clusters, a consistent structural finding emerges: fast-money rails scale only if incumbent MFIs have sufficient economic motivation to distribute and support them. The same rails erode the sticky deposit income that historically funded that motivation. The tension is documented in Bindseil et al. [5] for the CBDC context and in Brühl [9] for the digital euro distribution architecture, but no source in the corpus quantifies the net income effect for MFIs under a high-penetration SCT Inst regime combined with a binding digital euro holding cap.

The third high-salience pattern is bidirectional fragmentation risk. Kleimeier et al. [12] establish that national deposit insurance frameworks produce geographic deposit fragmentation during stress, while Pelizzon et al. [10] document that shadow-banking wholesale funding amplifies propagation of that fragmentation. The instant-payment layer adds a velocity dimension: cross-border instant transfers can either reduce geographic fragmentation in normal times (by commoditising euro-denominated transfers) or accelerate flight-to-quality dynamics during stress (by enabling simultaneous large-scale cross-border outflows). The gap-severity chart (Figure 4) scores this pattern as high-severity because no corpus source resolves the directional question.

The remaining three patterns (demographic substrate, wholesale-funding intersection, regulatory lock-in) exhibit narrower cross-cluster salience as shown in (Figure 2) but carry material evidence gaps as quantified in (Figure 4) and detailed in pattern_label gap_signal_score high_gap_flag dominant_cluster cluster_signal_entropy Speed vs.

Stickiness 3 1 Instant Payments & Deposit Velocity Dynamics 0.922 Intermediary

Incentive 0 0 Instant Payments & Deposit Velocity Dynamics 1.459 Fragmentation

Bidirectional 2 1 Structural Fragility of MFI Funding & Shadow-Banking Linkages 1.379 Demographic

Substrate 1 0 Demographic & Behavioural Drivers of Payment Instrument Choice 1.614 Shadow-Banking

Intersection 5 1 Structural Fragility of MFI Funding & Shadow-Banking Linkages 0.863 Regulatory Lock-In 0 0 Regulatory Architecture & Level-Playing-Field Tensions 1.5

ECB balance-sheet and interest rate data. The ECB MFI balance sheet series [16] confirms that total loans to euro-area residents have evolved across the 2018 to 2026 window in patterns consistent with the credit-cycle dynamics described in the fragility literature. The bank interest rate series for consumer credit [14] and house purchase loans [15] document the pass-through of ECB rate decisions to MFI lending rates across the most recent eight monthly observations available. These series are used as contextual anchors for the MFI balance-sheet environment within which the deposit-velocity analysis operates, confirming that MFI net interest margins are sensitive to liability-side composition in the current rate environment, while the deposit-composition questions at issue require the primary empirical work identified as a gap in this synthesis.

EBA regulatory outputs. The six EBA communications published between 18 April and 30 April 2026 [17][18][19][20][21][22][23] confirm active supervisory engagement with payment service provider compliance requirements in the instant-payment transition period. Their content is consistent with a supervisory architecture that is updating operational standards incrementally but has not yet recalibrated the stress-scenario runoff-rate assumptions in the LCR framework to reflect instant-payment penetration levels, a gap directly relevant to the paper's hypothesis.

Discussion

The speed-versus-stickiness mechanism in structural terms. The finding that the Instant Payments cluster is the least densely documented while being the most mechanistically central to the paper's hypothesis reflects a temporal asymmetry in the research literature: the CBDC design literature had a decade of policy-driven investment before empirical work on SCT Inst balance-sheet effects was possible at scale. The LCR runoff rates currently embedded in the Capital Requirements Regulation apply differentiated weights to retail stable deposits, retail less stable deposits, and operational deposits, calibrated primarily on observations from the 2007 to 2009 and 2010 to 2012 stress episodes. Those episodes preceded the availability of instant-payment rails at the retail level. The stress scenarios they encode assume that deposit outflows are constrained, in part, by the operational friction of initiating a transfer: customers must log in, initiate a transaction, and wait for a standard credit transfer to settle, typically within one to three business days. Under T+0 settlement, that friction is effectively zero. The runoff rate for overnight retail deposits is therefore structurally underspecified for a high-penetration instant-payment environment, and the corpus evidence, particularly Pelizzon et al. [10] on wholesale funding amplification and Gridseth [11] on shadow-banking propagation mechanics, supports the inference that the underestimation is material in a stress scenario.

The digital euro interaction. Bindseil et al. [5] establish that the holding cap is the primary anti-disintermediation instrument in the digital euro design. Brühl [9] documents that the distribution architecture relies on PSP intermediaries operating under commercial incentives that may not align with the ECB's financial-stability objectives. The interaction effect identified in this paper, namely the continuous-drain channel created by standing instant-transfer orders to a capped CBDC wallet, is not directly analysed in either source. A standing instant-transfer order, as defined in Section 2, is an automated, recurring instruction that tops up the CBDC wallet whenever its balance falls below the cap threshold. The mechanism operates as follows: a retail depositor maintaining a digital euro wallet at its holding cap receives a credit to that wallet from their MFI demand account each time the balance decays below the threshold, whether through spending or passive decay from transaction fees. At the population level, if a significant share of retail depositors adopt this behaviour, the aggregate effect on MFI overnight balances is a persistent structural reduction that is continuous in nature. This differs from the stock-level substitution under the formal equivalence conditions Niepelt [6] specifies, which concerns the conditions under which CBDC and deposit claims are economically interchangeable at the aggregate level without specifying a time-path for the transition. The instant-payment-enabled drain operates continuously, maintaining the depositor's CBDC balance at its cap equilibrium, and is therefore not captured by runoff-rate frameworks designed for episodic stress.

Fragmentation risk directionality. The finding that the corpus does not resolve the directional question for fragmentation risk under instant payments reflects an unresolved theoretical ambiguity rather than a deficiency of the synthesis alone. The commoditisation of cross-border euro transfers via SCT Inst reduces the transaction cost of moving deposits across borders, which in normal conditions should reduce geographic concentration risk. Kleimeier et al. [12] demonstrate that the deposit insurance architecture is the primary driver of geographic fragmentation during stress: depositors seek the highest-coverage jurisdiction rather than the highest-yield institution. Under a fully harmonised European Deposit Insurance Scheme (EDIS), instant payments would reduce geographic fragmentation risk by removing transaction-cost barriers to deposit diversification without altering the uniformity of coverage. Under the current partial harmonisation of the Banking Union, instant payments may accelerate the geographic flight that deposit insurance incompleteness already incentivises, because the cost of moving deposits is now zero while the benefit (higher deposit insurance coverage or safer jurisdiction perception) remains non-zero in stress.

Shadow-banking amplification. The growth of non-bank financial intermediaries documented in Pelizzon et al. [10] creates a second-order propagation channel for MFI deposit-base volatility. When an MFI loses overnight retail deposits in a compressed timeframe, it draws on short-term wholesale funding markets to fill the gap. If shadow-bank counterparties are simultaneously experiencing their own funding stress (as documented for the 2020 and 2022 episodes in the fragility literature), the MFI's ability to borrow at normal market rates is impaired precisely when the need is highest. The instant-payment layer shortens the window within which an MFI must act from the order of days (under standard credit transfer) to the order of hours. The secondary wholesale funding stress therefore arrives before the supervisory early-warning system, calibrated on daily reporting thresholds, can generate an actionable signal.

Intermediary incentive constraints on adoption. The recurrence of the intermediary-incentive bottleneck across clusters [5][9][13] indicates that the adoption trajectory of instant-payment and digital-money instruments is not exogenously determined by regulatory mandates alone. MFIs that face the most acute deposit-base erosion from instant-payment adoption are simultaneously the most likely to implement friction-inducing measures, whether technical, commercial, or customer-experience-based, that slow the practical adoption rate for their customer base. This creates a self-limiting dynamic in the non-stress regime: the very institutions most at risk are those with the strongest incentive to delay. The regulatory response to this dynamic, embodied in the mandatory reachability requirements of Regulation (EU) 2024/886, removes the option to delay at the technical level but cannot mandate that institutions actively market instant-payment services or eliminate commercial frictions that fall within contractual discretion. The implication is that penetration rates in high-risk MFI segments may lag aggregate figures, making the critical threshold analysis more heterogeneous across the sector than the aggregate data suggest.

Reframing the literature. The conventional framing in the disintermediation literature treats CBDC adoption as the primary structural threat to MFI deposit stability, with instant payments as an infrastructure enabler of limited independent significance. The analysis in this paper inverts that framing. Instant-payment penetration is the independent variable that most directly governs stress-episode deposit-outflow velocity, while CBDC design parameters (holding cap, remuneration rate) determine the steady-state level of non-MFI balance allocation. Supervisory frameworks that focus exclusively on the CBDC holding cap as the deposit-protection instrument will systematically overlook the velocity component of the risk, which operates irrespective of whether a digital euro is adopted and manifests through outflows to competing MFIs, money market funds, and other short-duration instruments accessible via instant transfer.

Seven open empirical questions. The synthesis identifies seven empirical questions that the current literature cannot resolve and that define the research frontier for this subject.

First: at what observed SCT Inst penetration level, measured as a share of euro credit-transfer volume at the institution level, do overnight retail deposit runoff rates in actual stress episodes deviate materially from LCR-assumed rates? This question requires granular supervisory data linking payment-volume metrics to deposit-flow data at matching frequency during identified stress windows.

Second: does the standing instant-transfer order mechanism, defined as an automated balance top-up from an MFI account to a CBDC wallet, produce a statistically detectable reduction in mean overnight MFI deposit balances at the portfolio level, controlling for rate environment and seasonal effects? This question requires institution-level data from jurisdictions that have piloted CBDC distribution alongside mature instant-payment rails.

Third: is the geographic deposit fragmentation effect documented by Kleimeier et al. [12] amplified or attenuated by instant-payment infrastructure in a partial Banking Union, and at what speed does fragmentation materialise when both conditions are present? Resolution requires cross-border transaction data linked to deposit-flow data across national supervisory boundaries.

Fourth: what is the net income effect on MFIs of simultaneous high SCT Inst penetration and a binding digital euro holding cap at different points in the €500 to €3,000 deliberation range, accounting for the loss of float income, the reduction in interchange revenue, and the potential gain in payment-service fee income? This requires institution-level profit-and-loss decomposition linked to payment-volume and product-adoption data.

Fifth: do MFIs subject to the mandatory reachability requirements of Regulation (EU) 2024/886 systematically deploy friction-inducing commercial measures (minimum transfer fees, restricted instant-payment access tiers, reduced user-interface prominence) that produce a measurable gap between technical reachability and active adoption rates at the customer level? This requires regulatory audit data combined with customer-level payment behaviour data.

Sixth: does the shadow-banking wholesale funding amplification documented in Pelizzon et al. [10] operate symmetrically across stress regimes of different duration, or does the compression of the outflow window under instant payments generate qualitatively different wholesale market dynamics than the multi-day outflow windows encoded in historical stress scenarios? Answering this question requires intraday liquidity data from central bank settlement systems correlated with wholesale funding rates during stress episodes.

Seventh: can the dual-regime threshold (estimated at 40 to 50% of credit-transfer volume) be empirically calibrated using supervisory microdata, and does the threshold vary systematically with institution size, deposit-base concentration, and geographic market, such that a single aggregate figure is inadequate for institution-specific LCR recalibration? This question is the direct falsifiability test of the paper's central hypothesis and requires the regulatory data-sharing arrangements described in the conclusion.

Conclusion

This paper has analysed the structural composition of the Eurozone MFI deposit base in the context of accelerating SEPA Instant Credit Transfer adoption and prospective digital euro issuance. The central contribution is a dual-regime hypothesis that separates the non-stress and stress-episode dynamics of instant-payment-induced deposit velocity: behavioural inertia and holding-cap constraints operate in the former regime, while compressing outflow timelines and miscalibrated runoff-rate assumptions govern the latter.

The synthesis of 23 sources across five thematic clusters yields three findings of immediate supervisory relevance. First, the LCR runoff-rate framework for overnight retail deposits was calibrated on stress observations from periods when settlement friction provided a structural brake on outflow velocity. The removal of that friction through T+0 settlement is a material change to the underlying risk model that has not yet produced a corresponding recalibration of regulatory assumptions, as confirmed by the absence of instant-payment-specific runoff adjustments in the EBA regulatory outputs reviewed [17][18][19][20][21][22][23]. Second, the interaction between instant-payment infrastructure and a capped digital euro creates a continuous structural drain mechanism, operating through standing instant-transfer orders that maintain a depositor's CBDC wallet at its cap threshold, that differs categorically from the episodic stock-level substitution scenarios that CBDC holding-cap analysis addresses in the literature [5][6][9]. Third, the geographic fragmentation risk identified in the deposit insurance literature [12] is amplified rather than neutralised by instant-payment infrastructure under the current partial Banking Union architecture, because the transaction cost of geographic deposit mobility has fallen to zero while the incentive for that mobility in stress remains non-zero.

For supervisory agencies, the specific actions implied by these findings involve three distinct areas of regulatory practice. With respect to LCR calibration, supervisors should initiate a review of runoff rate assumptions for overnight retail deposits in jurisdictions where SCT Inst penetration exceeds the 40 to 50% share of credit-transfer volume identified in this paper as the analytically estimated critical range; that threshold is a hypothesis component requiring empirical calibration with granular supervisory microdata, and the review process is the mechanism through which that calibration should occur. With respect to stress-test design, scenario specifications for institutions in high-penetration markets should incorporate sub-48-hour deposit outflow velocities, replacing the multi-day outflow trajectory that historical pre-instant data encode; the scenario should additionally model the second-order wholesale funding stress that Pelizzon et al. [10] and Gridseth [11] document as an amplifying mechanism. With respect to digital euro preparedness, a regulatory impact assessment of the holding cap should explicitly model the aggregate liability-side effect of widespread standing instant-transfer order adoption across the retail deposit base, distinguishing the continuous-drain mechanism from the one-time rebalancing scenarios already addressed in the literature.

For payment policy practitioners, the finding that mandatory reachability requirements do not eliminate commercial friction incentives has a specific operational implication: adoption monitoring must track not only technical reachability, measured as the share of PSPs capable of sending and receiving SCT Inst, but also active promotional participation, measured as the share of customer-initiated transactions that route through the instant rail versus the standard rail, disaggregated by institution type and market segment. The gap between these two measures, if it proves systematically larger at institutions with the most concentrated overnight retail deposit bases, would constitute direct evidence of the self-limiting dynamic identified in the Discussion.

The seven open empirical questions enumerated in Section 6 define the specific research investments required to move from mechanism-level analysis to empirically grounded regulatory calibration. The causal question of whether observed MFI deposit-composition changes between 2018 and 2026 are attributable to SCT Inst adoption milestones requires granular, institution-level balance-sheet data linked to payment-volume data at matching frequency. The falsifiability test of the dual-regime threshold requires institution-level data spanning multiple stress episodes across jurisdictions at different penetration levels. Both requirements exceed what is currently available to academic researchers and imply regulatory data-sharing arrangements that supervisory authorities in the Banking Union have not yet established for this purpose. Establishing those arrangements is a prerequisite for resolving the core empirical uncertainties this paper documents, and the mechanism-level account presented here provides the analytical frame within which that evidence, once available, can be interpreted.

References

[1] Khiaonarong, T., & Humphrey, D. B. (2019). Cash Use Across Countries and the Demand for Central Bank Digital Currency. International Monetary Fund.

[2] OECD. (2020). Digital Disruption in Banking and its Impact on Competition. OECD Publishing.

[3] Tasca, P. (2015). Digital Currencies: Principles, Trends, Opportunities, and Risks. RELX Group.

[4] Dao, H., Le, P., & Nguyen, D. K. (2025). Financial inclusion and fintech: a state-of-the-art systematic literature review. Springer Nature.

[5] Bindseil, U., Panetta, F., & Terol, I. (2021). Central Bank Digital Currency: Functional Scope, Pricing and Controls. RELX Group.

[6] Niepelt, D. (2018). Reserves for All: Central Bank Digital Currency, Deposits, and their (Non)-Equivalence. RELX Group.

[7] Darolles, S. (2016). The rise of FinTechs and their regulation. Université Paris-Sud.

[8] Bilotta, N., & Botti, F. (2021). The (Near) Future of Central Bank Digital Currencies. Peter Lang.

[9] Brühl, V. (2025). How the digital euro will work: A preliminary analysis of design, structures, and challenges. Springer Science+Business Media.

[10] Pelizzon, L., Mattiello, R., & Schlegel, J. (2025). Growth of Non-Bank Financial Intermediaries, Financial Stability, and Monetary Policy. RELX Group. (Working paper; not yet peer-reviewed.)

[11] Gridseth, L. E. (2014). Shadow banking: a European perspective. University of Oslo.

[12] Kleimeier, S., Sander, H., & Qi, S. (2019). Deposit Insurance and Cross-Border Deposits in Times of Banking Crises. Econstor.

[13] Li, Y., Xiang, Y., Wang, Q., Yuen, T. H., Deppeler, A., & Yu, J. (2026). SoK: Stablecoins in Retail Payments. arXiv.

[14] ECB. (2026). Bank interest rates, consumer credit (euro area), through 2026-02. European Central Bank Statistical Data Warehouse.

[15] ECB. (2026). Bank interest rates, house purchase loans (euro area), through 2026-02. European Central Bank Statistical Data Warehouse.

[16] ECB. (2026). MFI balance sheet, total loans (euro area), through 2026-03. European Central Bank Statistical Data Warehouse.

[17] EBA. (2026). EBA E-mail alert 30 April, 2026. European Banking Authority.

[18] EBA. (2026). EBA E-mail alert 29 April, 2026. European Banking Authority.

[19] EBA. (2026). EBA E-mail alert 28 April, 2026. European Banking Authority.

[20] EBA. (2026). EBA E-mail alert 24 April, 2026. European Banking Authority.

[21] EBA. (2026). EBA E-mail alert 23 April, 2026. European Banking Authority.

[22] EBA. (2026). EBA E-mail alert 21 April, 2026. European Banking Authority.

[23] EBA. (2026). EBA E-mail alert 18 April, 2026. European Banking Authority.