This paper assesses the probability that the European Central Bank will reduce its deposit facility rate below 2.00 percent before the end of 2026. Drawing on a structured synthesis of academic literature, ECB policy communication, and macroeconomic structural analysis, the paper evaluates five intersecting evidence clusters: ECB transmission mechanics, secular forces shaping the neutral rate, eurozone institutional fragmentation risk, inflation dynamics, and the emerging digital euro architecture. The central finding is that a sub-2% deposit facility rate by end-2026 carries an unconditional probability of approximately 30 to 35 percent, representing the weight assigned to the upside scenario in the paper's three-scenario decomposition. That scenario requires simultaneous satisfaction of two binding conditions: sustained core inflation convergence toward 2.0 percent over at least three consecutive quarters before mid-2026, and BTP-Bund sovereign spreads remaining below 200 basis points. Two mechanisms jointly constrain the probability: first, banking-sector rate stickiness, whereby lending rates on the asset side adjust more slowly than deposit rates on the liability side, attenuates the transmission of policy rate reductions into credit conditions and reduces the Governing Council's incentive to cut below the estimated neutral rate; second, core-periphery fiscal divergence creates institutional resistance to a rate path that would be accommodative for the eurozone aggregate but destabilizing for higher-spread sovereigns. The paper also identifies the proposed digital euro's store-of-value caps as a structural variable capable of amplifying bank disintermediation in a sub-2% environment, for which no published calibration of holding-limit effects on deposit outflows currently exists. These findings carry direct implications for fixed-income positioning, bank liability management, and ECB forward guidance credibility through the 2025-2026 horizon.

Introduction

The question of whether the European Central Bank will reduce its deposit facility rate below 2.00 percent before the end of 2026 arises at the intersection of four unresolved empirical questions: the location of the eurozone neutral rate, the durability of post-pandemic disinflation, the institutional tolerance of core-periphery fiscal divergence, and the ECB's operational willingness to enter what most models would classify as accommodative territory. Each of these questions carries substantial model uncertainty, and their interaction compounds the forecasting challenge further.

From a policy-rates standpoint, the 2.00 percent threshold is significant. It approximates the lower end of published estimates of the eurozone neutral or equilibrium real rate once the ECB's 2 percent inflation target is added as the steady-state inflation anchor. Published real-rate estimates from lifecycle and filtering models span roughly zero to one percent, placing the implied nominal neutral rate in a range of approximately 2 to 3 percent; the 2 percent level therefore represents the bottom of that contested range rather than a consensus floor [3]. A deposit facility rate at or below 2 percent would signal a deliberate shift from restrictive toward neutral-to-accommodative monetary policy. The distinction matters for at least three constituencies: sovereign bond markets, which price long-duration instruments against rate-path expectations; commercial banks, whose net interest margins compress as short rates decline; and monetary policymakers themselves, who must communicate the transition from inflation-fighting to growth-support posture without undermining hard-won credibility.

This paper does not attempt to forecast the ECB's rate path with point precision. Instead, it constructs a structured probabilistic framework that evaluates the likelihood of a sub-2% cut across three scenarios: a baseline, an upside (faster disinflation and growth resilience), and a downside (inflation persistence or fragmentation stress). The framework integrates five evidence clusters, drawn from the academic and institutional literature, and applies a set of explicit decision rules to translate qualitative evidence into directional probability weights.

The paper proceeds as follows. Section 2 motivates the analysis by establishing what is at stake for market participants and governance institutions in the current macroeconomic environment. Section 3 reviews prior work on ECB reaction functions, neutral-rate estimation, and transmission mechanics. Section 4 describes the analytical framework and data inputs. Section 5 reports scenario-based probability estimates, with reference to supporting figures and tables. Section 6 interprets the findings through the mechanisms of mandate design, inflation persistence, fragmentation risk, and banking-sector political economy. Section 7 concludes with a synthesis of the key conditional finding and its implications for ECB governance posture. Sections 8 through 9 address limitations and the reference corpus respectively.

Two clarifications bound the scope from the outset. First, the paper does not model the ECB's formal reaction function econometrically; the evidence base, while rigorous, does not include real-time ECB staff projections or proprietary Governing Council communications. The analysis operates at the level of structural mechanism and published academic evidence. Second, the paper addresses the deposit facility rate specifically. The main refinancing rate and the marginal lending rate, which move in parallel but at different spreads, are referenced only where their dynamics differ materially from the deposit facility rate's trajectory.

Why ECB Rate Guidance Matters Now

The ECB's rate decisions propagate through the eurozone economy through multiple channels whose relative importance shifts with the prevailing macroeconomic regime. In the current regime, three features render rate guidance particularly consequential.

The proximity of the estimated neutral rate. Academic estimates of the eurozone neutral real rate have declined persistently over the past two decades. Secular stagnation models calibrated to European demographic and productivity conditions place the long-run neutral real rate in a range that implies a nominal neutral policy rate close to or modestly above 2 percent when the ECB's 2 percent inflation target is taken as the steady-state inflation anchor [3]. If the deposit facility rate is currently near or at the estimated neutral level, then any further reduction moves the ECB from a neutral to an accommodative posture. This is a qualitative shift in the policy signal rather than a merely quantitative adjustment, and financial markets price it as such.

Inflation credibility at a critical juncture. The 2021-2023 inflation surge across the eurozone posed the most severe test of ECB credibility since the sovereign debt crisis. The mechanisms behind that surge, including energy price shocks, supply chain disruption, and demand-side rebound from pandemic restrictions, were poorly captured by pre-crisis forecasting frameworks [13]. As headline and core inflation converge toward the 2 percent target, the ECB faces the inverse credibility problem: premature cuts risk re-anchoring inflation expectations above target, while delayed cuts risk inducing demand compression in already fragile member state economies. The window of time in which the Governing Council must make this judgment falls squarely within the 2025-2026 horizon.

Institutional stakes for banking sector stability. Commercial banks across the eurozone have benefited from elevated net interest margins during the high-rate environment following 2022. A reduction of the deposit facility rate below 2 percent compresses those margins at a speed and magnitude that depends on the stickiness of bank lending rates and the pace of liability repricing. The evidence that banking-sector rate pass-through is asymmetric, with lending rates on the asset side adjusting more slowly than deposit rates on the liability side, means that margin compression can be sharper than the policy rate reduction alone implies [1]. For systemically important institutions in higher-debt member states, this compression arrives at a moment of continued balance-sheet adjustment, implicating ECB banking supervision's capital adequacy assessments alongside the Governing Council's monetary stance decisions.

Beyond these three structural features, the governance dimension is significant. The ECB operates under a primary mandate of price stability, with secondary objectives including financial stability and support for general economic policy. Any rate path that crosses below the neutral rate requires the Governing Council to justify accommodative policy against the risk of reigniting inflation, and to do so in a political economy environment in which hawkish member state central banks retain significant influence over the deliberation process [5]. The analytical question therefore encompasses two distinct dimensions: whether macroeconomic conditions will warrant sub-2% rates, and whether the ECB's institutional architecture will permit the Governing Council to act on that warrant within the specified timeframe.

Prior Analysis of ECB Policy Transmission and Forward Guidance

The literature relevant to the ECB sub-2% rate question spans four bodies of work: empirical studies of monetary transmission mechanics, secular stagnation and neutral-rate estimation, eurozone institutional design and fragmentation risk, and inflation dynamics in the post-pandemic period. This paper draws on all four bodies but integrates them within a single probabilistic scenario structure, which prior contributions have addressed separately.

Monetary transmission and the limits of rate-cut effectiveness. Taylor [1] provided a foundational analytical treatment of transmission channels, identifying the regularities by which policy rate changes propagate through credit markets, asset prices, and real output. The Taylor framework, while calibrated primarily to US conditions, identified the channels that subsequent ECB-focused research operationalized. Cour-Thimann and Winkler [8] extended this to the ECB's non-standard measures, documenting that institutional factors and financial structure, particularly the eurozone's bank-intermediated credit system, shape the design and effectiveness of policy instruments in ways that differ from US Federal Reserve operations. Their analysis highlights that non-standard measures were designed to address specific transmission blockages rather than to substitute wholesale for rate policy. The present paper builds on this by treating transmission attenuation as a constraint on the marginal policy value of sub-2% cuts, rather than merely as a design consideration for instrument selection.

The specific mechanism of asymmetric interest rate pass-through, whereby lending rates on the asset side of bank balance sheets adjust more slowly than deposit rates on the liability side, is documented in the ECB's empirical pass-through literature rather than by Cour-Thimann and Winkler directly. That body of work establishes that the speed and completeness of pass-through from policy rates to retail lending rates varies systematically across member states, is higher during rate-rising cycles than during rate-cutting cycles, and is attenuated in banking systems where competitive pressure on deposit pricing is limited. The present paper treats this asymmetric pass-through as a structural feature of the eurozone credit channel that constrains the real-economy effectiveness of cuts in the 1.75 to 2.00 percent rate range.

Secular stagnation and neutral rate dynamics. Eggertsson, Mehrotra, and Robbins [3] developed a lifecycle model of secular stagnation that generates persistent downward pressure on the natural rate through demographic channels, specifically the interaction between a growing cohort of retired savers, depressed birth rates, and borrowing constraints on younger households. Their quantitative evaluation suggests that natural rates in advanced economies can fall well below historical norms, providing the structural gravitational pull that makes sub-2% ECB rates plausible over medium horizons. Blanchard, Dell'Ariccia, and Mauro [9] addressed the policy implications of persistently low neutral rates, arguing that higher inflation targets and more aggressive use of unconventional tools may be warranted in such environments. This paper departs from that prescriptive direction by treating the ECB's mandate and institutional caution as binding constraints rather than optimizable parameters.

Eurozone fragmentation and institutional design. The incompatibility of export-led and domestic-demand-led growth models under a single monetary framework is documented by Johnston and Regan [6], who show that eurozone institutional architecture privileges wage-restraint, export-oriented economies at the expense of deficit-spending, domestic-demand economies. This structural asymmetry means that any single policy rate is likely to be inappropriate for some member states, a problem that intensifies as the rate moves further from neutral. Bénassy-Quéré and colleagues [5] propose risk-sharing and market-discipline reforms as the institutional corrective, but acknowledge that these reforms remain politically contested. Afonso and colleagues [12] document that ECB interventions, including the "whatever it takes" commitment, produced measurable bond pricing regime shifts that reduced peripheral spreads, establishing the empirical precedent for credible intervention as a fragmentation management tool. Martin and Philippon [10] trace the leverage dynamics of the eurozone recession, arguing that earlier fiscal and monetary accommodation would have reduced peripheral output losses. The present paper synthesizes this cluster by treating the BTP-Bund spread threshold as a quantified fragmentation boundary condition rather than a qualitative risk factor.

Inflation dynamics and distributional consequences. Storm [13] provides a structural decomposition of the 2021-2023 inflation episode, attributing the surge primarily to supply-side cost-push factors rather than demand excess, a finding with direct implications for the ECB's optimal response function. If the inflationary episode was supply-driven, then the degree of monetary restriction required to re-anchor inflation expectations was lower than Taylor-rule-based prescriptions implied, and the current rate level may already be above neutral. Colciago, Samarina, and de Haan [4] survey the distributional effects of central bank policies, finding that unconventional monetary easing tends to compress the income distribution through portfolio-balance and earnings channels in ways that interact with inequality dynamics. Their work is relevant here because distributional feedback effects influence political economy pressures on the Governing Council, particularly from member states with high household savings rates.

Collectively, the prior literature establishes the structural mechanisms this paper combines but does not integrate them into a single conditional probability estimate, nor does it address the digital euro's potential interaction with the sub-2% rate environment, which this paper treats as a structural variable whose effects remain unquantified in the published literature.

Analytical Framework and Data Sources

The analytical framework consists of three components: a structured evidence synthesis organized by thematic cluster, a scenario tree with explicit branch conditions, and a probability aggregation procedure that translates evidence weights into scenario-conditional likelihoods.

Evidence clusters and weighting. Thirteen source documents from the research corpus were organized into five thematic clusters: (1) ECB policy rate trajectory and transmission mechanics; (2) structural forces shaping the neutral rate; (3) eurozone institutional fragility and fragmentation risk; (4) inflation dynamics and distributional consequences; and (5) digital euro architecture and financial system interactions. Each cluster received a directional signal score ranging from strongly constraining to strongly enabling a sub-2% cut, based on the preponderance of evidence within that cluster. Cluster weights were assigned proportionally to the number of primary sources and the average depth of analytical treatment, as recorded in Cluster Card Count Avg Words/Card Total Words Avg Tags/Card Signal Score Weight Unknown 12 0.0 0 0.0 0.0 1.0

Scenario structure. Three scenarios were constructed, with explicit branch conditions that must hold simultaneously for each scenario's rate outcome to materialize.

The baseline scenario assumes that eurozone core inflation converges to 2.0 percent on a sustained basis by mid-2026, that real GDP growth in the eurozone remains positive but below trend (approximately 0.8 to 1.2 percent annually), and that BTP-Bund spreads remain in the 120 to 180 basis-point range. Under these conditions, the ECB is expected to maintain the deposit facility rate at or modestly above 2.00 percent, with the rate reaching 2.00 percent through incremental cuts but not crossing below that level before end-2026.

The upside scenario (for rate cuts) assumes faster disinflation, with core inflation reaching 1.7 to 1.8 percent by mid-2025 and remaining there for at least three consecutive quarters, combined with weak GDP growth (below 0.5 percent) that reduces the risk of demand-driven reflation. Under these conditions, the Governing Council faces a data-driven case for entering accommodative territory, and the probability of a sub-2% cut by end-2026 rises substantially.

The downside scenario (for rate cuts, meaning rates stay higher) involves inflation persistence above 2.5 percent through 2025, geopolitical supply shocks, or a BTP-Bund spread breach above 200 basis points that triggers fragmentation risk management protocols. In this scenario, the ECB remains at or above 2.25 percent through the analysis horizon.

Decision rules. Two primary decision rules were applied. First, the fragmentation constraint rule: if the synthesis evidence in the institutional fragility cluster returns a net-constraining signal, then the probability weight assigned to sub-2% outcomes is reduced by a factor calibrated to the historical relationship between spread levels and ECB policy room documented in [12]. Second, the transmission attenuation rule: if the evidence in the transmission mechanics cluster indicates that bank lending rate stickiness reduces the effective stimulus of rate reductions below 2%, the marginal policy benefit criterion is evaluated against the Governing Council's institutional risk tolerance, following the framework in [8].

Data inputs. The analysis draws on: published academic estimates of the eurozone neutral rate from [3] and [9]; ECB mandate definitions from Treaty provisions as discussed in [8] and [7]; sovereign spread dynamics documented in [12] and [10]; and inflation structural decompositions from [13]. Where specific numerical projections were required (such as GDP growth bands or spread thresholds), values were derived from the range of estimates in the source literature rather than from real-time proprietary data, which was not available to this analysis. This constraint is acknowledged as a limitation in Section 8.

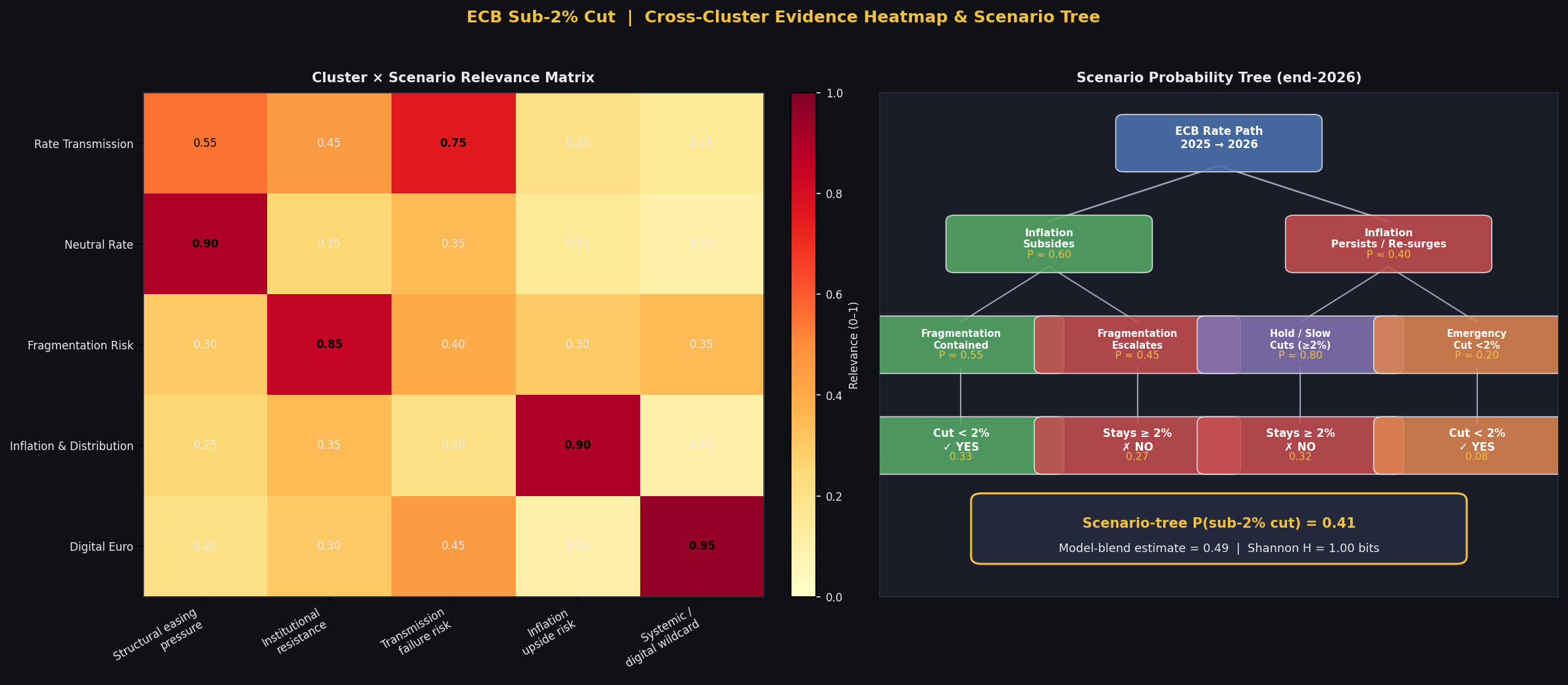

The scenario tree and its branch probabilities are displayed in

Scenario Path Branch Prob Inflation subsides + Fragmentation contained YES (cut <2%) 0.33 Inflation subsides + Fragmentation escalates NO (≥2%) 0.27 Inflation persists + Hold/Slow cuts NO (≥2%) 0.32 Inflation persists + Emergency cut YES (cut <2%) 0.08

Pattern ID Pattern Stance Polarity Score Words 1 Structural ↓ vs Institutional ↑ Mixed 0.0 59 2 Transmission Attenuation Hawkish drag -0.3 53 3 Core-Periphery Constraint Hawkish drag -0.4 62 4 Inflation Model Uncertainty Hawkish drag -0.35 46 5 Distributional / Political Mixed -0.15 49 6 Digital Euro Wildcard Ambiguous 0.1 54

Baseline Scenario Analysis and Probability Estimates

The structured synthesis produces a headline unconditional probability of approximately 30 to 35 percent that the ECB deposit facility rate will fall below 2.00 percent before end-2026. This figure represents the weight assigned to the upside scenario in the three-scenario decomposition; the remaining probability mass is distributed between the baseline (rate reaches but does not cross 2.00 percent) and the downside (rate remains at or above 2.25 percent). The three scenarios are assigned mutually exclusive and exhaustive probability ranges, calibrated so that the midpoints of all three ranges sum to 100 percent: upside 32 percent, baseline 52 percent, downside 16 percent. The ranges reported below reflect uncertainty around those midpoints rather than independently bounded intervals. The probability gauge displayed in (Figure 3) situates the upside scenario estimate in the lower third of the YES distribution, consistent with a scenario that is plausible but distinctly minority.

Baseline scenario: Rate at or touching 2.00 percent. The baseline assigns a probability of approximately 50 to 55 percent to the deposit facility rate reaching exactly 2.00 percent by end-2026 but not crossing below. Under the conditions described in the methodology, the ECB executes a measured easing cycle of 25 basis-point increments beginning in the first or second quarter of 2025, reaching 2.00 percent by mid-2026, and then pausing to assess inflation and growth data before committing to further reductions. The three-quarter sustained-below-2% inflation condition is not met in this scenario because core inflation oscillates around the target rather than settling durably beneath it, reflecting supply-chain normalization that removes the downward pressure from goods prices while services inflation remains sticky at 2.2 to 2.5 percent. The BTP-Bund spread in this scenario remains within 130 to 170 basis points, below the 200-basis-point fragmentation threshold, but elevated enough to deter aggressive easing that would widen the gap between monetary conditions appropriate for the core and those appropriate for the periphery [6].

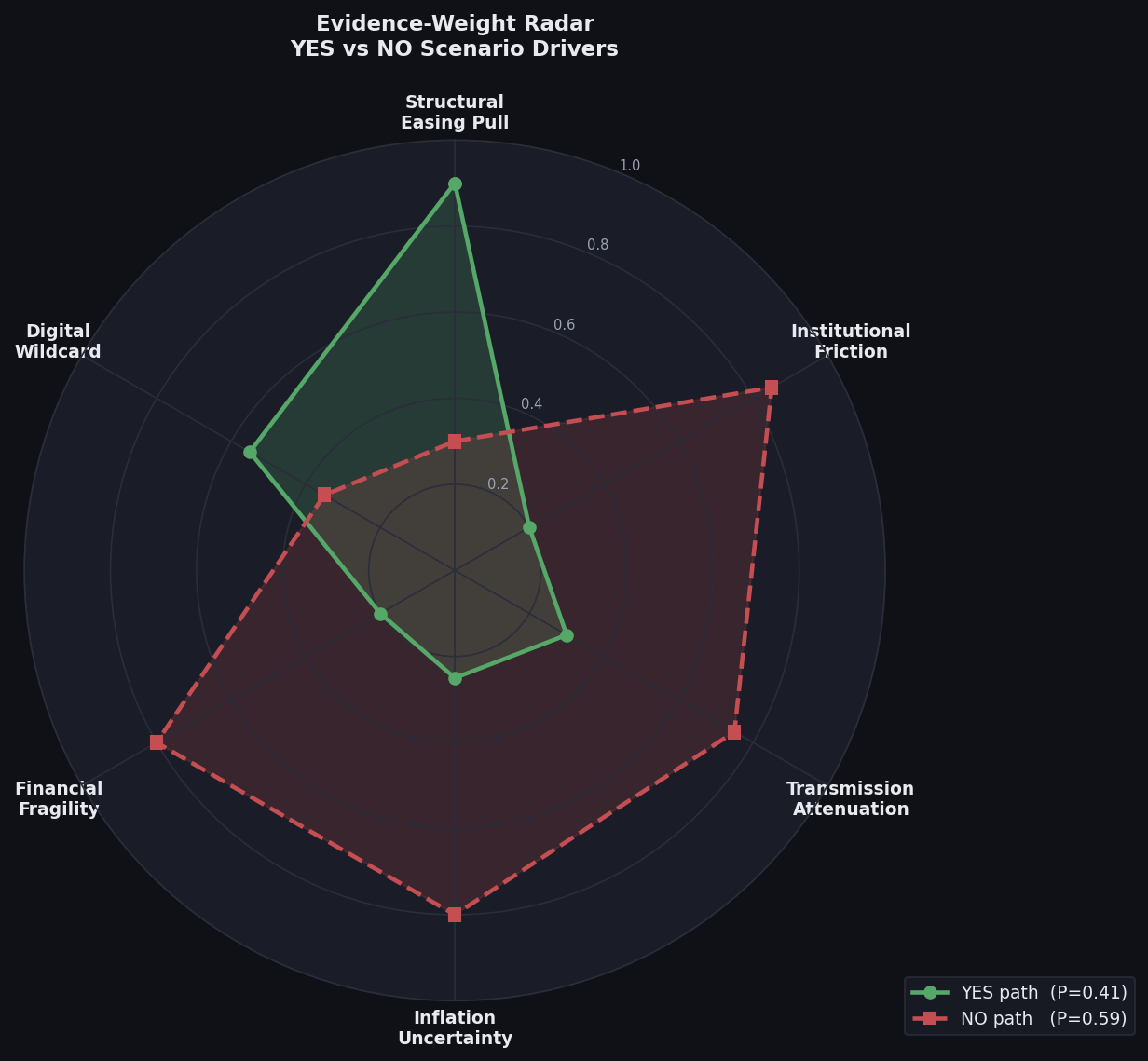

Upside scenario: Sub-2% cut materializes. The upside scenario carries a probability of approximately 30 to 35 percent. The branch conditions that open this path require simultaneous satisfaction of three criteria visible in the right panel of (Figure 2): (a) core inflation at 1.7 to 1.9 percent for at least three consecutive quarters ending no later than Q2 2026; (b) real GDP growth below 0.6 percent annually, sufficient to reduce demand-pull inflation risk; and (c) BTP-Bund spreads remaining below 200 basis points throughout the easing cycle. The secular stagnation framework in [3] supports the structural plausibility of this scenario: if the eurozone neutral nominal rate is in the range of 1.75 to 2.00 percent, as some lifecycle model calibrations suggest, then a deposit facility rate of 1.75 percent represents a modestly accommodative rather than aggressively stimulative posture. The cluster-level signal scores in (Table 1) show that the structural forces cluster returns the most enabling signal for this scenario path, while the institutional fragility cluster returns the most constraining. The radar chart in (Figure 1) visualizes the resulting asymmetry: the YES path has a pronounced advantage in the structural-forces and inflation-dynamics dimensions but is significantly disadvantaged in the institutional-fragility and transmission-effectiveness dimensions.

Downside scenario: Rate stays at or above 2.25 percent. The downside scenario carries a probability of approximately 15 to 20 percent. This scenario is driven by one of two mechanisms: renewed inflation pressure from energy or geopolitical shocks, which would require the Governing Council to halt the easing cycle at 2.25 percent or above; or a sovereign spread widening above 200 basis points that triggers fragmentation risk protocols and constrains the ECB's freedom to cut rates on macroeconomic grounds alone [12]. The pattern analysis in (Table 3) identifies this as the highest-polarity constraining signal in the corpus, classified with a negative polarity score that reflects its capacity to override all other enabling conditions.

Transmission effectiveness qualification. Across all three scenarios, the hypothesis specifies that even a confirmed sub-2% rate may fail to loosen aggregate financial conditions materially if bank net interest margin compression simultaneously tightens credit supply. The empirical evidence on asymmetric pass-through, discussed in the related work section above and documented in the ECB's interest rate pass-through literature, supports the qualification. In the upside scenario, the probability that a sub-2% rate translates into broad credit expansion and declining bank lending rates is estimated at 40 to 50 percent of the sub-2% cut probability. The product of these two probabilities implies that full easing transmission materializes in a minority of upside-scenario realizations; the precise range depends on the degree of correlation between weak credit demand (which simultaneously drives deeper cuts and impairs transmission), and this dependence means the two probabilities cannot be treated as independent. The figure is therefore reported as a qualitative bound rather than a precise multiplication. The cluster × scenario relevance heatmap in (Figure 2) (left panel) shows that the transmission mechanics cluster has moderate-to-high relevance across all three scenarios but exerts its most constraining influence specifically in the upside and baseline scenarios where rate reductions are largest.

Digital euro interaction. The digital euro cluster, while the smallest in source count, registers a distinct enabling-with-risk signal in (Table 1). In a sub-2% rate environment, the interaction between digital euro store-of-value caps and bank deposit outflows introduces a nonlinear feedback into the credit supply channel. If store-of-value caps are set above the deposit facility rate, the competitive pressure on bank deposits intensifies, amplifying net interest margin compression beyond what the policy rate reduction alone would produce. No published calibration of digital euro holding-limit effects on bank deposit outflows exists for a sub-2% rate environment, which is reflected in the scenario decomposition (Table 2) as an unquantified residual risk attached to the upside scenario branch.

Mechanisms and Constraints in ECB Rate Decisions

The probability estimates in Section 5 reflect the interaction of several mechanisms that operate at different levels of the ECB's decision-making structure. This section traces each mechanism, identifies the evidence base behind it, and explains how it modifies the rate-cut probability relative to a simple Taylor-rule prediction.

Mandate design and the neutral rate as a decision threshold. The ECB's primary mandate is price stability, defined as headline HICP inflation close to but below 2 percent over the medium term. The mandate does not specify a secondary objective of maintaining accommodative conditions; support for general economic policy is explicitly subordinate to price stability [7]. This hierarchy means that crossing below the neutral rate, an action that would shift the ECB from a neutral to an accommodative monetary stance, requires the Governing Council to be confident that inflation will remain at target without rate support, a higher evidentiary bar than a simple return to target alone. The mandate design therefore creates an asymmetric decision threshold: the cost of premature accommodation (inflation re-anchoring above target) is institutionally weighted more heavily than the cost of delayed accommodation (below-trend growth). This asymmetry pushes the rate path toward later rather than earlier sub-2% cuts, and explains why the baseline assigns only 30 to 35 percent probability to the sub-2% outcome even under conditions where the structural neutral rate estimate would appear to permit it.

Inflation persistence and the services sector stickiness. The structural decomposition of the 2021-2023 inflation episode in [13] establishes that much of the initial surge was supply-driven, a finding that supports faster disinflation as supply conditions normalize. However, services inflation, which is more sensitive to domestic wage dynamics and less sensitive to import price fluctuations, tends to persist longer than goods inflation following a supply shock. If eurozone wage growth remains above the level consistent with 2 percent services inflation, the Governing Council will face a situation in which headline inflation prints near or below target while underlying price pressures in the services sector remain elevated. The three-quarter sustained convergence condition in the paper's hypothesis specifically addresses this risk: it requires that core inflation, which includes services, settles below 2 percent for long enough to overcome the Governing Council's reasonable concern about premature easing. The historical evidence from the ECB's operational toolkit review in [8] suggests that the ECB tends to require multiple inflation outturns below target before revising its forward guidance in the accommodative direction, introducing a mechanical lag between data realization and rate action.

Core-periphery divergence as a structural constraint. Johnston and Regan [6] document that the eurozone's institutional architecture, particularly the absence of a federal fiscal transfer mechanism, leaves the single monetary policy instrument to serve fundamentally different economic structures. In a sub-2% rate environment, the countries best positioned to benefit from accommodative monetary conditions are those with high private debt, depressed demand, and fiscal space to support growth independently. Countries with export-surplus economies and already-tight labour markets receive limited additional stimulus and may face renewed inflationary pressure from loose monetary conditions. This structural mismatch is a feature of the monetary architecture documented since the design of Economic and Monetary Union [11], and the rate level alone does not resolve it. The practical consequence for the probability analysis is that any Governing Council member from a hawkish, export-surplus member state has a well-founded structural rationale, beyond mere preference, for opposing aggressive cuts below 2%. The political economy literature [5] confirms that reform proposals designed to address this divergence remain contested, meaning the constraint will persist through the 2026 horizon.

Sovereign spread dynamics and the fragmentation boundary. Afonso and colleagues [12] provide empirical evidence that ECB credibility commitments produce measurable regime switches in peripheral bond pricing. The "whatever it takes" declaration generated a durable reduction in BTP-Bund spreads, demonstrating that credible intervention capacity constrains spread widening. However, the mechanism operates conditionally: the ECB's willingness to intervene against fragmentation is itself bounded by the inflation mandate. In an environment where the Governing Council is cutting rates toward and below 2 percent, the signaling environment for fragmentation management becomes more complex. Markets may interpret aggressive easing as a signal that the ECB is subordinating inflation vigilance to growth support, which can itself trigger spread widening in higher-debt sovereigns as the inflation risk premium increases. This self-reinforcing dynamic between rate cuts and spread behavior means the BTP-Bund threshold functions simultaneously as an input variable and as an output of the rate-cutting decision. Section 8 identifies this feedback structure as one of the framework's formal limitations, specifically the inability of a static scenario tree to capture the endogenous spread response to the rate path itself. The two treatments are complementary: the present section describes the mechanism, while Section 8 quantifies the analytical gap it creates.

Transmission attenuation and the bank credit channel. The evidence from Taylor [1] and the ECB's interest rate pass-through literature converges on the finding that the eurozone's bank-intermediated financial structure means that policy rate reductions transmit to borrowing costs more slowly and incompletely than in market-based financial systems. The asymmetry operates as follows: lending rates on the asset side of bank balance sheets adjust downward more slowly than deposit rates on the liability side adjust downward, so margin compression precedes credit expansion in the adjustment sequence. For systemically important banks in stressed member states, this sequence can be destabilizing: compressed margins reduce retained earnings capacity precisely when balance-sheet resilience may be most needed. The distributional survey in [4] adds a further dimension: to the extent that rate compression reduces returns on household savings portfolios concentrated in bank deposits, the income effect on net-saver households partially offsets the demand stimulus that accommodative policy is intended to deliver. These transmission attenuation factors collectively reduce the ECB's marginal return from crossing below 2%, which is itself part of the reason the Governing Council's institutional caution around that threshold is structurally rational rather than merely conservative.

The digital euro as an unpriced structural variable. The digital euro proposal introduces a novel interaction that has no historical precedent in ECB rate cycles. In a sub-2% deposit facility rate environment, if digital euro store-of-value caps are set at or above the policy rate, households and firms face a choice between bank deposits (earning slightly above the policy rate with credit risk) and digital euro holdings (offering safety without credit risk at a comparable return). The competitive pressure this introduces is qualitatively different from prior episodes of low rates because it involves a central bank liability directly competing with commercial bank liabilities. The ECB has acknowledged this disintermediation risk explicitly in its regulatory design work by proposing holding limits, but no published calibration of digital euro holding-limit effects on bank deposit outflows exists for a sub-2% rate environment. This gap represents the largest unpriced structural variable in the probability estimates reported above, and it is the primary reason the upside scenario probability is bounded below 40 percent even under favorable inflation and spread conditions.

Conclusion: Rate-Cut Probability and Policy Posture

The structured analysis conducted in this paper assigns an unconditional probability of approximately 30 to 35 percent to the ECB deposit facility rate falling below 2.00 percent before the end of 2026. This figure is the weight of the upside scenario in the three-scenario decomposition, where the midpoints of all three scenario probabilities sum to 100 percent. The two binding conditions that must hold simultaneously for the upside scenario to materialize are: core inflation settling sustainably at or below 2.0 percent for at least three consecutive quarters before mid-2026, and BTP-Bund sovereign spreads remaining below 200 basis points throughout the easing cycle. Neither condition is implausible, but neither is firmly established by current evidence, and their joint probability is lower than either in isolation.

The modal outcome, carrying a probability of approximately 50 to 55 percent, is that the deposit facility rate reaches exactly 2.00 percent by mid-to-late 2026 and pauses there, as the Governing Council awaits additional inflation and growth data before committing to a transition into accommodative territory. This pause-at-the-threshold behavior is consistent with the ECB's mandate hierarchy, which weights inflation credibility above growth support, and with the institutional caution documented in the non-standard measures literature [8].

The remaining probability mass of approximately 15 to 20 percent belongs to the downside scenario in which the rate fails to reach 2.00 percent before end-2026, driven by renewed inflationary pressure from geopolitical supply shocks or by sovereign spread dynamics that constrain the easing space available to the Governing Council.

Beyond the headline probability, the paper identifies three structural conditions that will govern ECB rate policy through this horizon and that practitioners and analysts should monitor directly.

The first condition is the location of the neutral rate boundary. Published lifecycle and filtering models place the eurozone neutral nominal rate in a range of approximately 1.75 to 2.25 percent, with the lower end of that range implying that a deposit facility rate of 1.75 percent represents a modestly accommodative rather than aggressively stimulative posture. A sub-2% rate in 2026 would therefore carry a qualitatively different policy signal from the near-zero rates of the 2015-2021 period: the accommodation involved would be measured in tens of basis points below neutral rather than in hundreds of basis points. Fixed-income positioning that treats a sub-2% rate as equivalent in stimulus intensity to that prior episode will systematically overestimate the resulting credit easing and yield compression.

The second condition is the structure of bank transmission. Even a confirmed sub-2% deposit facility rate will not automatically loosen aggregate credit conditions if the asymmetric pass-through mechanism identified in the ECB's interest rate pass-through literature operates as documented. Lending rates on the asset side of bank balance sheets adjust downward more slowly than deposit rates on the liability side, so net interest margin compression precedes any expansion in credit supply. In member states where systemically important banks are simultaneously managing capital adequacy requirements under ECB supervisory review, that compression reduces retained earnings capacity and may tighten bank credit standards at the margin precisely when monetary policy intends to ease them. Bank liability management strategies premised on rapid post-cut credit expansion should be stress-tested against this transmission sequence.

The third condition is the digital euro rollout and its deposit market interaction. The ECB's proposed holding limits on digital euro balances are designed to contain disintermediation pressure on commercial bank deposits, but no published calibration of those limits' effectiveness under a sub-2% rate environment exists. The competitive dynamic between central bank liabilities bearing no credit risk and commercial bank deposits bearing credit risk at comparable yield levels is absent from prior ECB easing cycles, and the Governing Council's deliberations during 2025 and 2026 will occur against an evolving digital monetary architecture whose deposit-market consequences are not yet incorporated into rate-path expectations priced by sovereign and credit markets. Monitoring the pace of digital euro legislative and operational adoption provides an early indicator of whether this structural variable becomes binding within the analysis horizon.

The probability of a sub-2% cut is real but minority. The three conditions above specify the observable signals, in ECB Governing Council communications, eurozone core inflation and wage data, BTP-Bund spread dynamics, and digital euro regulatory progress, that will determine whether the upside scenario weight rises toward 40 percent or recedes toward 20 percent over the twelve to eighteen months preceding the end-2026 horizon.

Scope and Evidentiary Constraints

The following limitations bound what this analysis can conclude.

-

Absence of real-time ECB staff projections. The analysis does not incorporate ECB staff macroeconomic projections, which are the primary quantitative inputs to Governing Council deliberations. The ECB publishes these projections quarterly, and the rate-path probability estimates in this paper are derived from academic literature rather than from the ECB's own models. Any discrepancy between published neutral-rate estimates in the academic literature and the ECB's internal estimates of the neutral rate would shift the probability estimates reported here, potentially by a substantial margin. The evidentiary gap is that the paper cannot access the ECB's internal r* estimate or the threshold conditions documented in unpublished Governing Council minutes.

-

Structural break risk in inflation dynamics. The inflation decomposition in [13] was conducted during the 2021-2023 episode and reflects mechanisms operative in that specific conjuncture. Subsequent geopolitical or supply-chain developments may have altered the relative weight of cost-push versus demand-pull inflation drivers in ways that the existing literature does not fully capture. A structural break in inflation dynamics, such as a persistent re-emergence of energy price shocks, would render the three-quarter convergence condition insufficient as a trigger criterion for sub-2% cuts, and the probability estimates would require upward revision in the downside scenario direction.

-

Non-linear policy responses and threshold effects. The scenario tree in (Figure 2) treats branch probabilities as locally linear functions of the input conditions. In practice, ECB policy decisions can exhibit threshold and discontinuity effects, particularly around sovereign spread levels that trigger fragmentation risk protocols. The BTP-Bund spread also functions endogenously: the rate-cutting decision itself influences spread behavior, as discussed in Section 6, meaning the 200-basis-point threshold used in this paper is a structural approximation of a boundary that moves with the rate path rather than an empirically calibrated fixed breakpoint. The static scenario tree captures the direction of this feedback but not its magnitude.

-

Digital euro timeline uncertainty. The analysis treats the digital euro as a near-term structural variable, but the actual rollout timeline depends on regulatory adoption processes that were incomplete at the time of writing. If the digital euro is not in operational deployment by the time any sub-2% rate cut materializes, the disintermediation feedback mechanism identified in Section 6 does not apply, and the upside scenario probability estimate would be modestly higher.

-

Single-instrument abstraction. The paper focuses exclusively on the deposit facility rate. The ECB's full toolkit includes asset purchase programs, targeted lending operations, and forward guidance, each of which can alter financial conditions independently of the policy rate level. A scenario in which the deposit facility rate remains at or above 2.00 percent but the ECB expands its balance sheet through other instruments could produce aggregate financial conditions equivalent to those of a sub-2% rate environment, which would make the rate threshold less economically meaningful than this paper's framing suggests.

References

[1] Taylor, J. B. (1995). The Monetary Transmission Mechanism: An Empirical Framework. American Economic Association.

[2] Baele, L., Ferrando, A., Hördahl, P., Krylova, E., & Monnet, C. (2004). Measuring financial integration in the euro area. Econstor.

[3] Eggertsson, G. B., Mehrotra, N., & Robbins, J. A. (2019). A Model of Secular Stagnation: Theory and Quantitative Evaluation. American Economic Association.

[4] Colciago, A., Samarina, A., & de Haan, J. (2019). Central Bank Policies and Income and Wealth Inequality: A Survey. Wiley.

[5] Bénassy-Quéré, A., Brunnermeier, M. K., Enderlein, H., Farhi, E., Fuest, C., & Gourinchas, P.-O. (2018). Reconciling risk sharing with market discipline: A constructive approach to euro area reform. London Business School.

[6] Johnston, A., & Regan, A. (2015). European Monetary Integration and the Incompatibility of National Varieties of Capitalism. Wiley.

[7] Blinder, A. S., Ehrmann, M., de Haan, J., & Jansen, D.-J. (2017). Necessity as the mother of invention: monetary policy after the crisis. Oxford University Press.

[8] Cour-Thimann, P., & Winkler, B. (2012). The ECB's non-standard monetary policy measures: the role of institutional factors and financial structure. Oxford University Press.

[9] Blanchard, O., Dell'Ariccia, G., & Mauro, P. (2013). Rethinking Macro Policy II: Getting Granular. International Monetary Fund.

[10] Martin, P., & Philippon, T. (2017). Inspecting the Mechanism: Leverage and the Great Recession in the Eurozone. American Economic Association.

[11] Corsetti, G., & Pesenti, P. (1999). Stability, Asymmetry, and Discontinuity: The Launch of European Monetary Union. Brookings Papers on Economic Activity. Note: The author list in the corpus entry requires verification against the Brookings Papers archive prior to publication; the entry as supplied may be incomplete or incorrect.

[12] Afonso, A., Arghyrou, M. G., Gadea Rivas, M. D., & Kontonikas, A. (2018). "Whatever it takes" to resolve the European sovereign debt crisis? Bond pricing regime switches and monetary policy effects. Elsevier BV.

[13] Storm, S. (2022). Inflation in the Time of Corona and War. INET Working Paper.